A Research Analysis on the Strategic Vulnerabilities of Incumbent Smartphone Giants in the Age of Artificial Intelligence

Section 1: A Familiar Pattern of Disruption

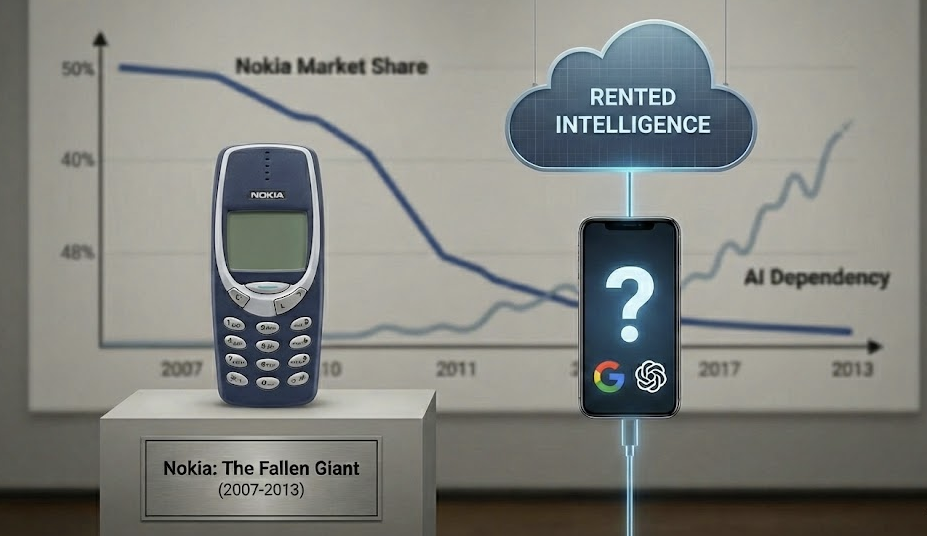

The history of the mobile industry is defined by a series of “extinction events” where hardware dominance was rendered irrelevant by a fundamental shift in the primary interface. In 2007, Nokia sat at the absolute zenith of the mobile world with a 48.7% global market share-a position of seemingly insurmountable dominance built over decades of engineering excellence and brand loyalty (International Data Corporation [IDC], 2013). By the second quarter of 2013, that figure had collapsed to 3.1%. Within six years, the world’s undisputed mobile leader had become a cautionary footnote, selling its devices division to Microsoft for €5.44 billion-a fraction of its former value (Microsoft Corporation, 2013). This unprecedented fall illustrates that engineering excellence offers no protection when a company fails to control the primary interface of its era.

Today, Apple and Samsung control approximately 39% of global smartphone shipments combined, with Apple claiming 20% and Samsung 19% of the market in 2025 (Counterpoint Research, 2026). Their devices are ubiquitous, their ecosystems entrenched, their brand loyalty seemingly unshakeable. Yet beneath this veneer of invincibility lies a troubling parallel to Nokia’s final years: neither company has built its own flagship artificial intelligence.

Today, as we enter the “Agentic AI” era, Apple and Samsung face a similar threat: they are increasingly “renting” the intelligence layer (the new interface) from third parties like Google and OpenAI rather than owning it. For the first time in two decades, the companies that define the smartphone experience may not control the most important layer of it.

This wouldn’t be the first time incumbents underestimated a shift in how humans interact with technology.

Section 2: The Conquerors and the Vanquished

To understand the stakes of the current AI transition, one must first examine how Apple and Samsung achieved their present dominance-and what their victories reveal about the nature of technological disruption.

The Fall of the Old Guard

The early 2000s mobile landscape was dominated by names that now evoke nostalgia rather than innovation. Nokia, at its peak, held over 50% of the U.S. smartphone market and 20% globally, with its devices considered synonymous with mobile communication itself (Harvard Business School, 2018). BlackBerry (then Research in Motion) controlled the corporate communication sphere, with its secure email functionality making it indispensable to business professionals-so much so that users coined the term “CrackBerry” to describe their addiction (Wharton School of Business, 2015).

Each of these companies possessed formidable advantages: established manufacturing capabilities, carrier relationships, loyal customer bases, and deep engineering expertise. Yet each fell victim to a fundamental misunderstanding of what would matter next.

Nokia lost the interface. The company’s leadership initially dismissed Apple’s touchscreen iPhone, with co-CEO Jim Balsillie insisting that users preferred physical keyboards. When Nokia belatedly released the touchscreen Storm in 2008, it was plagued with technical failures and poor user experience-a rushed response to a threat they had refused to acknowledge (Cognitive Market Research, 2025). Nokia’s smartphone market share fell from over 50% in 2007 to effectively 0% by 2016 (Statista, 2017).

BlackBerry lost the developer ecosystem. While Apple and Google built thriving app marketplaces that transformed smartphones into platforms for infinite possibility, BlackBerry’s proprietary operating system remained hostile to third-party development. The company controlled 20% of the smartphone market in 2009; by 2016, it sold only 207,900 devices in a single quarter-a market share rounded to 0.0% (Gartner, 2017).

How Apple and Samsung Won

Apple’s victory came from controlling the interface. The iPhone, introduced in 2007, was not merely a phone with a touchscreen-it was a complete reimagination of how humans interact with mobile computing. The multi-touch interface, combined with the App Store’s ecosystem launched in 2008, created a platform where third-party developers could extend functionality infinitely. Apple controlled the hardware, the operating system, the interface paradigm, and the application marketplace. This vertical integration created what would become the most valuable company in history.

Samsung’s success followed a different path but achieved similar ends. Rather than challenging Android, Samsung embraced it, becoming Google’s most important hardware partner while dominating the premium Android segment. Samsung invested heavily in manufacturing capabilities, particularly display and memory technologies, creating component advantages that competitors could not easily replicate. The Galaxy line, launched in 2010, grew to become the best-selling Android smartphone family globally.

| Brand | 2007 Market Share | 2025 Market Share | Outcome |

| Nokia | ~48% | <1% | Vanquished: Sold mobile division to Microsoft. |

| BlackBerry | ~20% | 0.0% | Vanquished: Lost the developer ecosystem battle. |

| Apple | ~3% (Initial launch) | 20% | Conqueror: Reclaimed #1 spot with 248 million shipments. |

| Samsung | ~7% | 19% | Conqueror: Maintained #2 spot with 241 million shipments. |

Key Drivers of the 2025 Dominance

- Apple’s Record Year: In 2025, Apple emerged as the global leader for the first time in over a decade, capturing a record one-quarter of all shipments in the final quarter of the year. This growth was fueled by the massive success of the iPhone 17 series across both mature and emerging markets.

- Samsung’s Resilience: Samsung maintained a strong second position with 19% market share. Its success was driven by the steady performance of the Galaxy A series in mid-range segments and high demand for the premium Galaxy S25 and Z series foldables.

- Industry Profits: Together, Apple and Samsung accounted for nearly 40% of all global shipments in 2025 and continued to claim the vast majority of the industry’s total profits.

Both companies understood a crucial truth: the value in mobile technology had shifted from hardware specifications to ecosystem integration. The smartphone was no longer a device but a platform-and whoever controlled the platform controlled the user relationship.

Each of these fallen giants didn’t lose because they lacked technology. They lost because they failed to control the next interface.

Section 3: The Fourth Industrial Revolution

The World Economic Forum defines the Fourth Industrial Revolution (4IR) as the ongoing transformation characterized by artificial intelligence, automation, and the fusion of physical, digital, and biological worlds (Schwab, 2016). Unlike previous industrial revolutions that changed how we produce goods, 4IR is changing how we think, create, and interact with reality itself.

AI as Behavioral Shift, Not Merely Computational Upgrade

The significance of AI for mobile technology extends far beyond faster processors or more sophisticated features. It represents a fundamental transformation in the human-device relationship. The user no longer taps-they increasingly ask.

Gartner projects that worldwide end-user spending on generative AI smartphones will reach $298.2 billion by the end of 2025, representing 20% of total AI end-user spending (Gartner, 2025). IDC forecasts over 370 million GenAI smartphones shipped globally in 2025, comprising 30% of total smartphone shipments, with growth continuing at 73.1% year-over-year into 2026 (IDC, 2025). By 2028, IDC projects 912 million GenAI smartphone shipments, with AI-enabled devices comprising 70% of the market (IDC, 2024).

These statistics describe more than an upgrade cycle-they signal a paradigm shift. As Nabila Popal, Senior Research Director at IDC, noted, “The rapid incorporation of GenAI in smartphones is unprecedented in mobile history with market penetration expected to exceed 60% within the first three years” (IDC, 2024).

The Emerging AI Ecosystem in Mobile

The AI mobile landscape is evolving rapidly across multiple dimensions. Google’s Tensor chips, developed specifically for AI workloads, enable in-house features like Magic Editor and real-time translation that operate independently of cloud connectivity. Samsung’s partnership with Google Cloud, announced in January 2024, brought Gemini Pro and Imagen 2 to the Galaxy S24 series-making Samsung the first manufacturer to deploy these models on smartphone devices (Samsung Global Newsroom, 2024).

Apple Intelligence, announced at WWDC 2024, combines on-device processing using a 3-billion-parameter model with server-based computation through Private Cloud Compute (Apple Machine Learning Research, 2024). The system emphasizes privacy through on-device processing while integrating ChatGPT for complex queries through a partnership with OpenAI announced in June 2024 (OpenAI, 2024).

Experimental approaches are also emerging. Companies like Nothing and Humane are developing AI-centric wearables that challenge the smartphone form factor itself. OpenAI has announced plans to release its first hardware device in 2026, working with former Apple Chief Design Officer Jony Ive, with CEO Sam Altman describing it as “a radical departure” from current mobile technology (Built In, 2025).

The strategic question is not whether AI will transform mobile computing-that outcome appears certain. The question is who will own the intelligence layer that mediates the user relationship.

Yet, as AI surges forward, why are the market leaders playing catch-up with borrowed technology-and what does that mean for their throne?

Section 4: The Miss-Renting Intelligence Instead of Owning It

The competitive positions of Apple and Samsung in the AI era reveal a profound strategic vulnerability: both companies have chosen to integrate AI rather than own it. This distinction may prove decisive.

The Architecture of Dependency

Apple’s AI strategy has undergone a dramatic shift that underscores its fundamental reliance on external partners. In January 2026, Apple announced a multi-year partnership with Google to power its next-generation Apple Intelligence features, including the long-delayed upgraded Siri, using Google’s Gemini models and cloud technology (Google & Apple, 2026). This represents a pivotal move away from OpenAI, which Apple had partnered with in June 2024 to integrate ChatGPT into iOS.

The decision came after Apple evaluated options from OpenAI, Anthropic, and its own internal models. Apple determined that “Google’s AI technology provides the most capable foundation for Apple Foundation Models” (CNBC, 2026). The company rejected Anthropic due to high fees and found its own models struggling with hallucinations and latency on mobile silicon (MacRumors, 2025). Apple is reportedly paying Google approximately $1 billion annually for Gemini access.

Samsung’s dependency runs even deeper. The Galaxy AI suite was “the first smartphone equipped with Gemini Pro and Imagen 2 on Vertex AI” (Google Cloud, 2024). Samsung plans to double Gemini-powered devices to 800 million units by the end of 2026.

The result is striking: Google’s Gemini now powers AI features in both major mobile operating systems. As one analyst observed, this deal “cements Google as the ‘utility provider’ for the AI era, powering the two largest mobile operating systems on Earth” (Editorial GE, 2026).

The Existential Questions

Two scenarios threaten the current mobile duopoly. First: what happens if AI agents become hardware-agnostic? The smartphone becomes a commodity shell, and the user relationship transfers to whoever owns the intelligence layer.

Second: what happens if an AI-native company builds hardware? OpenAI has confirmed plans to launch its first device in 2026, with Jony Ive leading design (Mobile App Daily, 2026). Elon Musk continues signaling interest in an xAI-powered device (Teslarati, 2024). A vertically integrated AI-first phone would represent genuine disruption rather than iteration.

History suggests that when the interface changes, hardware dominance alone is not enough to stay relevant.

Section 5: Conclusion – The Price of Renting Intelligence

The smartphone industry’s history offers a clear and unforgiving pattern: dominant players fall when they fail to control technological transitions. Nokia dismissed touchscreens. BlackBerry ignored app ecosystems. Each possessed advantages that appeared insurmountable until they weren’t.

Apple and Samsung now face their own transition moment, but with a troubling distinction from their predecessors: they appear to recognize the threat yet remain unable or unwilling to address it. Both companies have chosen to rent intelligence rather than build it. Apple’s January 2026 pivot from OpenAI to Google Gemini did not represent a step toward independence; it merely changed landlords. Samsung’s plan to deploy Gemini across 800 million devices by year-end further entrenches its dependency on a company that also happens to be its primary platform provider and potential competitor.

The Dependency Trap

The parallels to Nokia’s position in 2007 grow more uncomfortable with each passing quarter. Nokia didn’t lack resources, engineering talent, or market presence. What Nokia lacked was ownership of the layer that would define the next era of mobile computing. Apple and Samsung find themselves in a strikingly similar position today.

When Apple, a company legendary for vertical integration and controlling every aspect of its user experience, must turn to Google to power its flagship AI features, something fundamental has shifted. When Samsung, the world’s largest smartphone manufacturer, cannot differentiate its devices without licensing intelligence from the same company that provides its operating system, the strategic vulnerability becomes existential.

The risk is not hypothetical. OpenAI has confirmed plans to launch hardware in 2026, with Jony Ive leading design. Elon Musk continues to signal interest in an xAI-powered device. These are not idle threats from underfunded startups; they represent well-capitalized, AI-native organizations that view the smartphone as a distribution problem to be solved rather than a core competency to be protected.

The Path Not Taken

Apple’s $162 billion cash position could fund transformative AI acquisitions. Samsung’s manufacturing capabilities could enable rapid deployment of proprietary AI silicon. Both companies possess the resources to build rather than rent. Yet quarter after quarter, they choose partnership over ownership, integration over innovation.

The justification is understandable: building frontier AI models requires billions in compute infrastructure, years of research, and tolerance for uncertain returns. Renting from Google offers immediate capability at predictable cost. But this calculus ignores the lesson of every previous platform transition: whoever controls the interface controls the user relationship, and whoever controls the user relationship captures the value.

A Probable Future

If current trajectories hold, the 2030s may witness a restructuring of the mobile industry that rivals the 2010s in magnitude. Google, already powering AI on both iOS and Android, could emerge as the true platform owner, with Apple and Samsung reduced to premium hardware assemblers. Alternatively, an AI-native entrant could achieve what seemed impossible for Nokia’s competitors in 2006: displacing incumbents by owning the layer that matters most.

Apple and Samsung are not destined for Nokia’s fate. They possess resources, ecosystems, and brand loyalty that could sustain them through significant disruption. But resources did not save Nokia. Ecosystems did not save BlackBerry.

What saved Apple in 2007 was recognizing that the interface was changing and having the courage to cannibalize its own iPod business to own the next platform. The question for today’s mobile giants is whether they possess that same clarity and courage, or whether they will continue renting intelligence until they discover, too late, that they have rented away their relevance.

Nokia didn’t believe a computer company could make phones. BlackBerry didn’t believe consumers would prefer touchscreens to keyboards. Today’s giants shouldn’t believe that renting AI from competitors is a sustainable strategy, or that hardware alone will protect them when the intelligence layer becomes the interface that users actually value.

The clock is ticking. The 1-trillion-parameter model Apple is reportedly building may arrive in late 2026, or it may not. Samsung shows no signs of reducing its Gemini dependency. Meanwhile, OpenAI’s device timeline advances, xAI’s compute capacity expands, and Google’s position as the intelligence provider for both major mobile platforms solidifies.

History does not repeat, but it rhymes. The companies that defined the smartphone era have perhaps three to five years to determine whether they will own the AI era or be disrupted by it. Based on current evidence, the latter outcome appears increasingly probable.

References

- Apple Machine Learning Research. (2024). Introducing Apple’s on-device and server foundation models. https://machinelearning.apple.com/research/introducing-apple-foundation-models

- Apple Machine Learning Research. (2025). Updates to Apple’s on-device and server foundation language models. https://machinelearning.apple.com/research/apple-foundation-models-2025-updates

- Built In. (2025). OpenAI’s new device: What we know so far. https://builtin.com/articles/openai-device

- CNBC. (2024, December 11). Apple launches its ChatGPT integration with Siri. https://www.cnbc.com/2024/12/11/apple-launches-its-chatgpt-integration-with-siri.html

- CNBC. (2026, January 12). Apple picks Google’s Gemini to run AI-powered Siri coming this year. https://www.cnbc.com/2026/01/12/apple-google-ai-siri-gemini.html

- CNN Business. (2026, January 12). Apple teams up with Google Gemini for AI-powered Siri. https://www.cnn.com/2026/01/12/tech/apple-google-gemini-siri

- Cognitive Market Research. (2025). A leading early smartphone manufacturer’s decline: A case study in the smartphone market’s rapid evolution. https://www.cognitivemarketresearch.com/blog/blackberry-s-decline-a-case-study-in-the-smartphone-market-s-rapid-evolution

- Counterpoint Research. (2026, January). Global smartphone market share: Quarterly. https://counterpointresearch.com/en/insights/global-smartphone-share

- Editorial GE. (2026, January). Apple Google Gemini deal: Why Alphabet beat OpenAI for Siri. https://editorialge.com/apple-google-gemini-deal-2026/

- Fortune. (2026, January 13). Why Google wins big in Apple AI deal, while OpenAI loses. https://fortune.com/2026/01/13/apple-ai-deal-with-google-gemini-means-for-google-apple-openai/

- Gartner. (2017). Chart: The terminal decline of BlackBerry. Statista. https://www.statista.com/chart/8180/blackberrys-smartphone-market-share/

- Gartner. (2025, September 9). Gartner says worldwide GenAI smartphone end-user spending to total $298 billion by the end of 2025. https://www.gartner.com/en/newsroom/press-releases/2025-09-09-gartner-says-worldwide-generative-artificial-intelligence-smartphone-end-user-spending-to-total-us-dollars-298-billion-by-the-end-of-2025

- Google. (2026, January 12). Joint statement from Google and Apple. https://blog.google/company-news/inside-google/company-announcements/joint-statement-google-apple/

- Google Cloud. (2024, January 17). Samsung and Google Cloud join forces to bring generative AI to Samsung Galaxy S24 series. https://www.googlecloudpresscorner.com/2024-01-17-Samsung-and-Google-Cloud-Join-Forces-to-Bring-Generative-AI-to-Samsung-Galaxy-S24-Series

- Harvard Business School. (2018, February 1). The rise and fall (and rise again?) of BlackBerry. Digital Innovation and Transformation. https://d3.harvard.edu/platform-digit/submission/the-rise-and-fall-and-rise-again-of-blackberry/

- International Data Corporation. (2013, July 25). Global market share held by Nokia smartphones from 1st quarter 2007 to 2nd quarter 2013. Statista. https://www.statista.com/statistics/263438/market-share-held-by-nokia-smartphones-since-2007/

- International Data Corporation. (2024). Worldwide generative AI smartphone shipments forecast to reach 70% of the market by 2028 with more than 360% growth in 2024. https://my.idc.com/getdoc.jsp?containerId=prUS52478124

- International Data Corporation. (2025, August 27). Worldwide smartphone market forecast to grow 1% in 2025, driven by accelerated 3.9% iOS growth. https://my.idc.com/getdoc.jsp?containerId=prUS53767725

- International Data Corporation. (2026, January). IDC: Smartphone shipments up 2.3% in Q4 2025, Apple is the clear winner. GSMArena. https://www.gsmarena.com/idc_smartphone_shipments_up_23_in_q4_2025_apple_is_the_clear_winner_-news-71096.php

- MacRumors. (2025, November 5). Apple’s new Siri will be powered by Google Gemini. https://www.macrumors.com/2025/11/05/apple-siri-google-gemini-partnership/

- McKinsey & Company. (2022, August 17). What is industry 4.0 and the Fourth Industrial Revolution? https://www.mckinsey.com/featured-insights/mckinsey-explainers/what-are-industry-4-0-the-fourth-industrial-revolution-and-4ir

- Microsoft Corporation. (2013, September 3). Microsoft to acquire Nokia’s devices & services business, license Nokia’s patents and mapping services. https://news.microsoft.com/source/2013/09/03/microsoft-to-acquire-nokias-devices-services-business-license-nokias-patents-and-mapping-services/

- Mobile App Daily. (2026, January). OpenAI is set to launch their first hardware device in 2026. https://www.mobileappdaily.com/news/openai-jony-ive-ai-device-2026

- NPR. (2024, June 11). Apple doubles down on artificial intelligence, announcing partnership with OpenAI. https://www.npr.org/2024/06/10/nx-s1-4999051/apple-artificial-intelligence-partnership-openai-chatgpt-siri-iphone

- OpenAI. (2024, June 10). OpenAI and Apple announce partnership. https://openai.com/index/openai-and-apple-announce-partnership/

- Samsung Global Newsroom. (2024, January 17). Samsung and Google Cloud join forces to bring generative AI to Samsung Galaxy S24 series. https://news.samsung.com/global/samsung-and-google-cloud-join-forces-to-bring-generative-ai-to-samsung-galaxy-s24-series

- Schwab, K. (2016, January 14). The Fourth Industrial Revolution: What it means and how to respond. World Economic Forum. https://www.weforum.org/stories/2016/01/the-fourth-industrial-revolution-what-it-means-and-how-to-respond/

- Statista. (2017). Market share held by Nokia smartphones 2007-2013. https://www.statista.com/statistics/263438/market-share-held-by-nokia-smartphones-since-2007/

- TechCrunch. (2026, January 12). Google’s Gemini to power Apple’s AI features like Siri. https://techcrunch.com/2026/01/12/googles-gemini-to-power-apples-ai-features-like-siri/

- Teslarati. (2024, June 11). Elon Musk reconsiders phone project after Apple Intelligence OpenAI integration. https://www.teslarati.com/elon-musk-reconsiders-phone-apple-intelligence-openai-chatgpt-integration/

- TIME. (2009). The 10 biggest tech failures of the last decade: Palm. https://content.time.com/time/specials/packages/article/0,28804,1898610_1898625_1898634,00.html

- Wharton School of Business. (2015, December 15). Victim of success: The rise and fall of BlackBerry. Knowledge at Wharton. https://knowledge.wharton.upenn.edu/podcast/knowledge-at-wharton-podcast/victim-success-rise-fall-blackberry/

This research paper represents analysis based on publicly available information as of January 2026. Market conditions and strategic positions may change rapidly in the technology sector