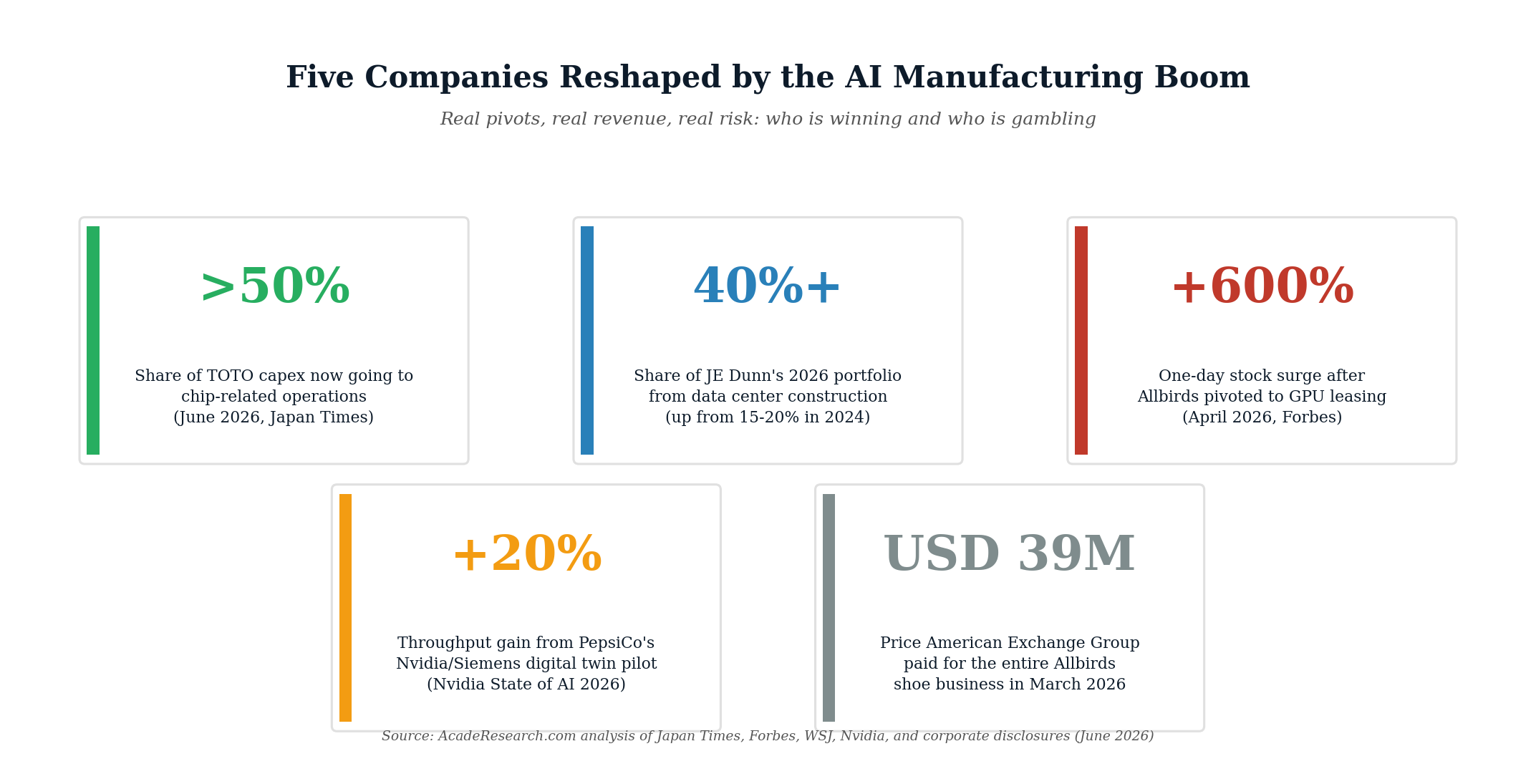

A 108-year-old Japanese toilet manufacturer is now sending more than half its capital expenditure to chip-fabrication ceramics. A construction firm has watched data centers swell from a fifth of its portfolio to nearly half in two years. A bankrupt shoe brand sold itself for $39 million and saw its empty shell trade up 600 percent on a press release. AI is reorganizing what it means to be a manufacturing business in 2026, and not every pivot is sound.

By Kenny Le

The most consequential change in industrial economics in 2026 is not happening inside an AI lab. It is happening in factories that produce toilets, ceramic discs, transformers, generators, and warehouse logistics services. The pattern is the same in every case: the AI infrastructure buildout has created a downstream supply-chain demand surge so large that companies in adjacent industries are reshaping their capital plans, customer bases, and corporate identities to capture a share of it. Some of the pivots are working. Others are pure financial engineering.

Five companies, viewed together, define the current state of the AI manufacturing transition.

Case 1: TOTO Pivots from Toilets to Chip Ceramics

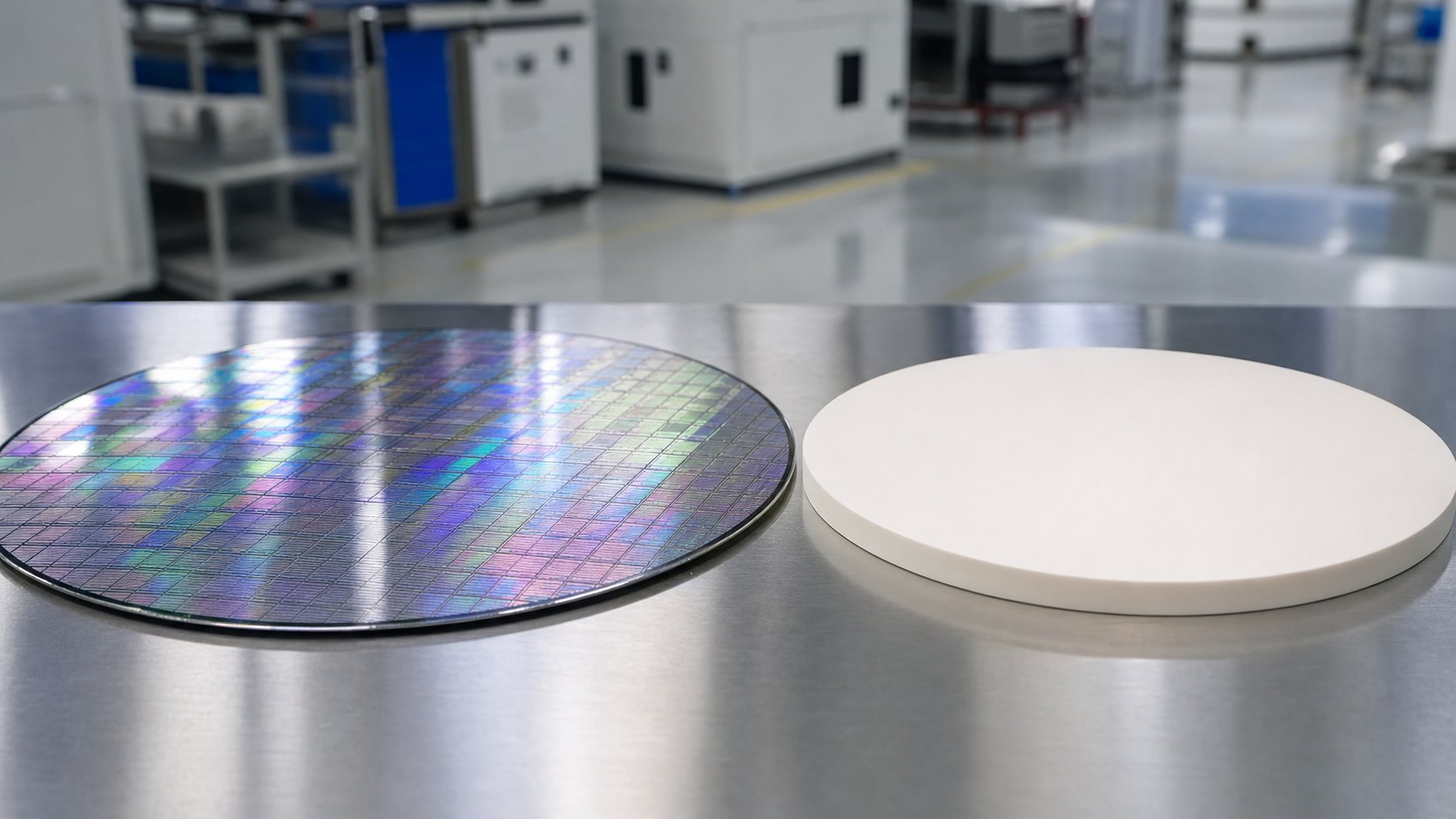

TOTO Ltd., the Japanese sanitary-ware manufacturer best known globally for its high-end toilets, told Bloomberg and Japan Times on June 2 to 3, 2026, that chip-related operations are now expected to account for more than half of the company’s total capital expenditure in coming years (Kiyohara, 2026). The driver: an unexpected surge in demand from chip-gear makers seeking TOTO’s century-old expertise in ceramics designed to withstand dirt particles, corrosive materials, and high temperatures.

The specific product TOTO has positioned around AI demand is the electrostatic chuck, a precision ceramic component that holds silicon wafers in place during chip fabrication. As Nvidia, TSMC, Samsung, SK Hynix, and the entire downstream chip-fab supply chain race to expand capacity for AI chips, the demand for electrostatic chucks and related ceramic components has compounded.

Chief Technology Officer Ryosuke Hayashi told the Japan Times that TOTO will prepare a production environment where “we can respond to demand properly” (Kiyohara, 2026). The quote is restrained. The reallocation is not. A company that has built its identity around bathroom fixtures for more than a century is now reorganizing its capital around the semiconductor industry’s needs.

The economic logic is sound. TOTO’s ceramic engineering capability is the asset, not the product category. AI demand has produced a customer base that values that capability more than the consumer market currently does. The pivot is not abandoning toilets; it is recognizing that the same precision-ceramics know-how can serve a far higher-margin customer.

Case 2: JE Dunn Construction Builds the AI Boom

JE Dunn Construction, a privately held Kansas City-based general contractor with a roughly $7 billion annual revenue base, is the kind of company that does not normally appear in AI coverage. It builds buildings. In a February 2026 Wall Street Journal feature, JE Dunn’s data-center division leader Chris Teddy explained that in 2024, the firm projected that data-center work would be 15 to 20 percent of its overall portfolio (Mickle & Higgins, 2026). That figure jumped to 30 percent in 2025. By 2026, Teddy projects data-center work will exceed 40 percent of total company activity.

The economic dynamic is straightforward. Hyperscaler data-center construction is the largest single capital-spending category in US industry in 2026, with Google, Microsoft, Meta, Amazon, Oracle, and emerging AI labs collectively committing hundreds of billions to new construction. JE Dunn does not need to invent a new product to participate. It simply needs to dedicate construction capacity to the new customer.

The risk is exactly that dedication. If data-center construction slows, due to capex pullback, electricity-grid limits, or a public-market repricing of AI valuations, JE Dunn’s revenue base becomes structurally exposed to a single demand source. Forty-percent customer concentration in a single industry is unusual for a general contractor and represents a material exposure that did not exist three years ago.

Case 3: PepsiCo Buys a Digital Twin from Nvidia and Siemens

PepsiCo, working with Siemens and Nvidia, is converting selected US manufacturing and warehouse facilities into high-fidelity 3D digital twins that simulate end-to-end plant operations and supply chains. Using Siemens’ Digital Twin Composer, PepsiCo can recreate every machine, conveyor, pallet route, and operator path with physics-level accuracy, enabling AI agents to simulate and refine system changes and identify up to 90 percent of potential issues before any physical modifications occur (Nvidia, 2026).

The reported business impact: a 20 percent increase in throughput on initial deployments, faster design cycles with nearly 100 percent design validation, and 10 to 15 percent reductions in capital expenditure for facility changes. The PepsiCo example is the inverse of TOTO and JE Dunn. PepsiCo is not pivoting toward AI customers. It is buying AI tools to make its existing manufacturing operations more efficient. The economic value is captured internally rather than through new revenue.

This is the model Deloitte’s 2026 Manufacturing Industry Outlook expects to define the next 24 months. The Deloitte survey of 600 manufacturing executives found that 80 percent plan to invest 20 percent or more of their improvement budgets in smart manufacturing initiatives (Deloitte Insights, 2026). The PepsiCo digital-twin program is the visible operational example of that investment posture.

Case 4 (Cautionary): Allbirds Becomes NewBird AI

Allbirds, the wool-shoe brand once valued at $4 billion when it went public at $15 per share in November 2021 and worn by Barack Obama and Leonardo DiCaprio, is now a financial vehicle in search of a business. In late March 2026, Allbirds divested its entire shoe business, brand, and product lines to American Exchange Group for $39 million (Markman, 2026). The remaining corporate shell, with $152 million in trailing revenue and $77 million in losses on the way out the door, announced it would rebrand as NewBird AI and pivot to leasing GPUs.

The stock surged nearly 600 percent in a single trading session after the announcement, from approximately $2.49 to an intraday high of $24.30, before declining 30 to 35 percent the following day. Forbes contributor Jon Markman documented what was actually happening: trading volume hit 288 million shares with over $5 million in net retail buying, against approximately 21 percent of the float sold short. The surge was, in Markman’s framing, a mechanical short squeeze fueled by retail enthusiasm surrounding the AI label rather than any substantive business shift.

The substance behind the pivot is thin. NewBird AI has announced a $50 million convertible financing deal with an undisclosed institutional investor, contingent on shareholder approval, intended for GPU purchases. The company has no customers, no identified partners, no acquired hardware, no disclosed customer pipeline, and no disclosed hardware acquisition timeline. It has also moved to rescind its public benefit corporation status and remove environmental conservation language from its charter, on the explicit logic that GPU leasing is an energy-intensive endeavor inconsistent with its prior commitments (Markman, 2026).

Markman’s blunt assessment: at current GPU prices, $50 million “would only secure a few hundred GPUs,” far below the scale required to operate a credible GPU-leasing business against competitors that have invested billions in fleets and data-center capacity.

What Separates the Pivots That Work from the Pivots That Don’t

Reviewing TOTO, JE Dunn, PepsiCo, and Allbirds against each other reveals a clear economic pattern. Three criteria separate substantive AI pivots from financial-engineering pivots.

The first is the existence of a transferable industrial capability. TOTO has spent a century engineering precision ceramics. JE Dunn has spent more than a century building large-scale construction projects. PepsiCo has built operational manufacturing expertise across decades. In each case, the AI opportunity reuses an existing core competence. Allbirds was a direct-to-consumer apparel brand whose competence in wool footwear has no observable transfer to the GPU-leasing industry.

The second is the presence of named customers with disclosed purchase commitments. TOTO is selling electrostatic chucks to specific chip-equipment makers. JE Dunn is building specific data-center projects for named hyperscaler clients. PepsiCo is consuming its own digital-twin output internally. Allbirds has no customers, no partners, no signed contracts, and no disclosed pipeline.

The third is the credibility of the capital plan. TOTO is reallocating already-existing capital expenditure toward a different product mix within its own factories. JE Dunn is shifting its labor and project allocation rather than building new infrastructure. PepsiCo is paying license fees to use someone else’s AI software inside its existing facilities. Allbirds’ $50 million convertible financing represents the entire capital base, will purchase only a few hundred GPUs, and is contingent on a shareholder vote that has not yet occurred.

When all three criteria are met, the AI pivot is an extension of an existing business model with a higher-margin customer attached. When none of the three criteria are met, the AI pivot is a ticker change.

The macro context. Hyperscaler capital expenditure on AI infrastructure reached approximately $320 billion in 2025 and is projected to approach $1 trillion by 2028. That spending cascades through the construction industry, the semiconductor equipment industry, the precision-component industry, the electrical-grid industry, and the industrial-services industry. The companies positioned to capture meaningful shares of that cascade are not new AI startups. They are 50- to 100-year-old industrial firms that already possess the supply-chain capabilities AI infrastructure now requires. The economic risk is concentration. Both customer concentration, as JE Dunn’s case illustrates, and product concentration, as TOTO’s chip-pivot illustrates, expose these firms to a single demand source whose long-term durability is not yet proven.

The Bottom Line

The AI boom is reshaping industrial business in two distinct ways at the same time. The substantive way is visible in TOTO’s reallocation of half its capex to chip ceramics, in JE Dunn’s portfolio shift from 15 percent to 40 percent data-center construction in two years, and in PepsiCo’s 20 percent throughput gains from internal digital-twin deployment. The performative way is visible in Allbirds’ overnight rebrand to NewBird AI, a corporate shell with no customers, no hardware, and $50 million that could only buy a few hundred GPUs but produced a 600 percent one-day stock surge. The economic logic separating the two is straightforward: real AI pivots reuse existing industrial capability, have named customers with signed commitments, and reallocate already-existing capital rather than depend on new financing. Financial-engineering pivots check none of those boxes. Investors, employees, and competitors evaluating any company’s “AI strategy” announcement in 2026 should apply that three-part test before assuming the pivot is real. The TOTOs and the JE Dunns of the manufacturing economy are reshaping themselves credibly around a multi-year demand surge. The Allbirds outcome, with its 30 to 35 percent same-day decline that followed the headline-driven spike, is what happens when the test is not applied.

References

Deloitte Insights. (2025, November 13). 2026 Manufacturing Industry Outlook. https://www.deloitte.com/us/en/insights/industry/manufacturing-industrial-products/manufacturing-industry-outlook.html

Kiyohara, M. (2026, June 3). Toilet-maker Toto hikes capital expenditures to meet AI demand for its ceramics. The Japan Times. https://www.japantimes.co.jp/business/2026/06/03/companies/toto-ai/

Markman, J. (2026, April 20). How $39 million shoe company Allbirds turned into an AI company. Forbes. https://www.forbes.com/sites/jonmarkman/2026/04/20/how-39-million-shoe-company-allbirds-turned-in-to-an-ai-company/

Mickle, T., & Higgins, T. (2026, February 5). Meet the non-tech firms betting big on the AI boom. The Wall Street Journal. https://www.wsj.com/business/meet-the-non-tech-firms-betting-big-on-the-ai-boom-5b17d340

Nvidia. (2026, March 9). State of AI 2026: How AI is driving revenue, cutting costs and boosting productivity. Nvidia Blog. https://blogs.nvidia.com/blog/state-of-ai-report-2026/