As prediction market trading volume surges toward $325 billion in 2026, two radically different companies are competing for dominance: Kalshi, the federally licensed exchange fighting state governments in court, and Polymarket, the crypto-native disruptor that returned to the United States after a four-year regulatory exile. Their divergent business models, funding strategies, and regulatory philosophies may define the shape of a new financial asset class.

Executive Summary

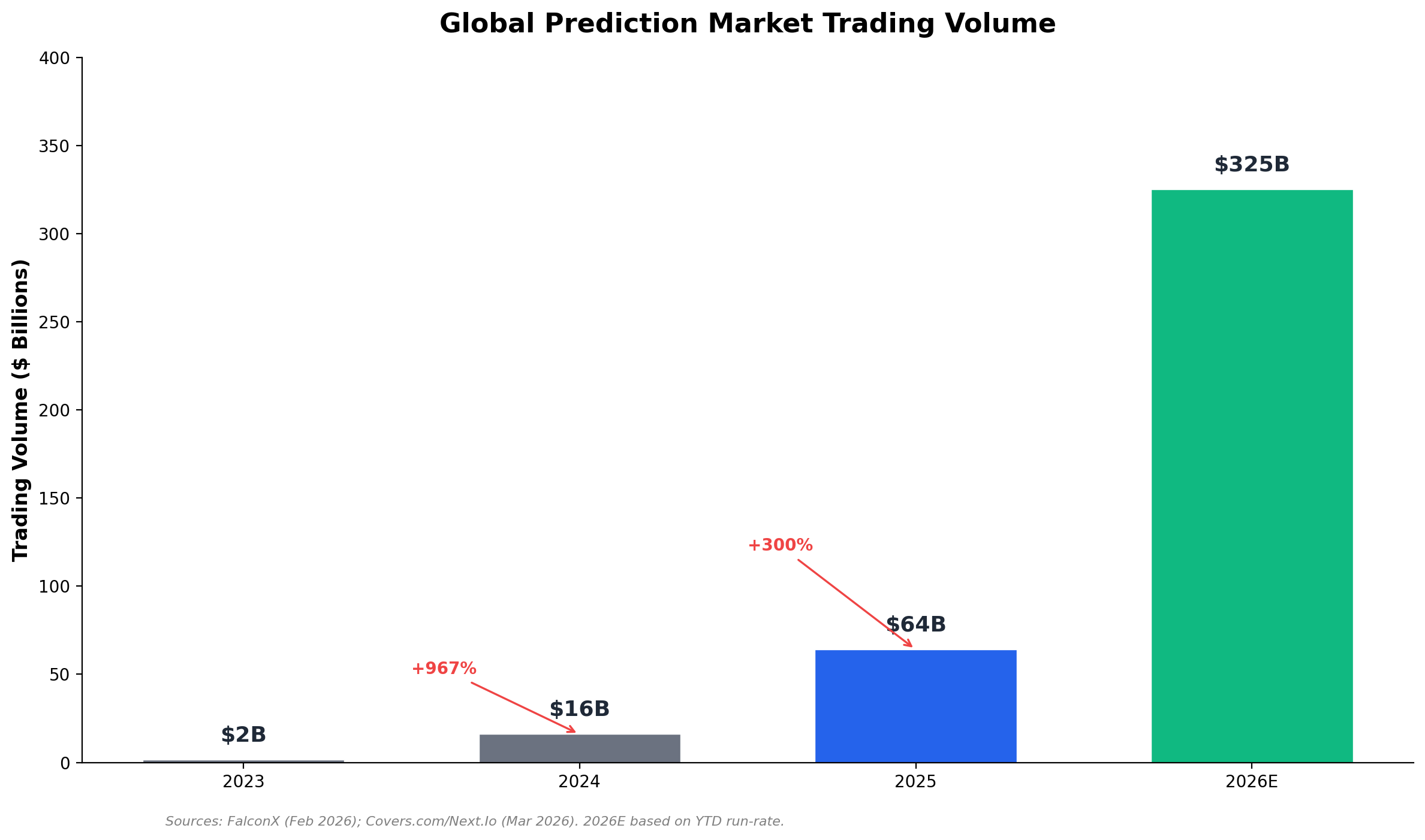

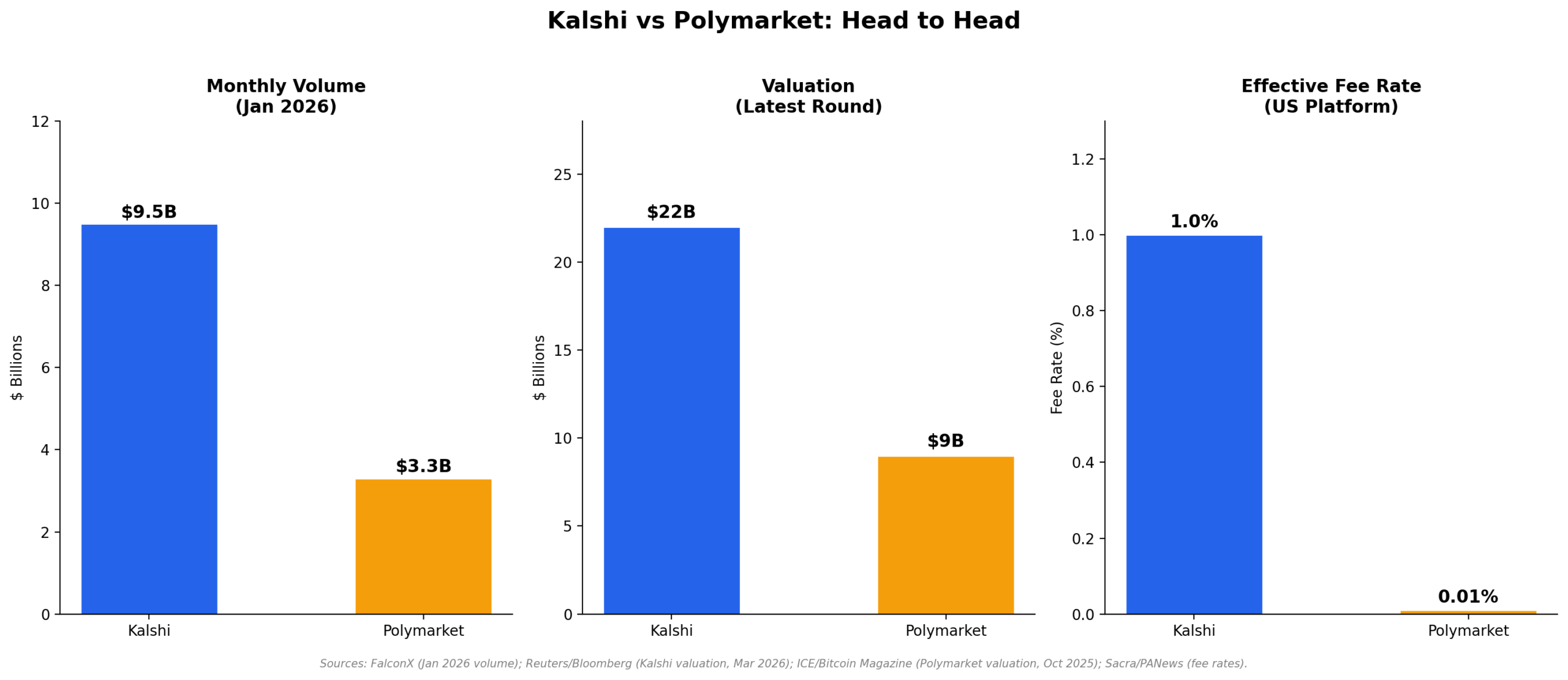

The prediction market industry reached an inflection point in 2025, with global trading volume hitting $64 billion, a nearly fourfold increase from 2024, according to data compiled by FalconX (2026). Two companies sit at the center of this transformation: Kalshi, a federally designated contract market (DCM) valued at $22 billion as of March 2026 (Reuters, 2026), and Polymarket, a blockchain-native platform backed by Intercontinental Exchange (ICE) at a $9 billion valuation (Bitcoin Magazine, 2025).

These companies are not merely competitors in a market. They represent two distinct and largely incompatible theories about what prediction markets are, who they serve, and how they should be governed. Kalshi bets on regulatory legitimacy as a competitive moat; Polymarket bets on liquidity, network effects, and a forthcoming token economy. Both are entering the mainstream simultaneously, and the tension between their models will shape the next decade of event-driven finance.

This analysis examines each company’s business model, revenue structure, regulatory positioning, user demographics, and strategic trajectory, with particular attention to the legal battles that could determine whether the industry thrives or fragments along state lines.

Section 1: The Prediction Market Explosion

1.1 Growth Trajectory

The scale of prediction market growth in 2025 and early 2026 is difficult to overstate. According to research published by FalconX (2026), global prediction market trading volume reached $64 billion in 2025, representing a 4x sequential increase from 2024. At the current year-to-date run-rate as of early 2026, volumes are on pace to exceed $325 billion for the full year. Drawing analogies to the exponential growth of perpetual futures markets in cryptocurrency, the same report estimates that prediction market volumes could exceed $1.1 trillion by 2030.

The daily volume record of $701.7 million was set in early 2026 (AInvest, 2026), a figure that would have seemed implausible just eighteen months prior. Monthly trading volume increased more than a hundredfold from early 2024, when the sector was still relatively obscure, to late 2025, jumping from under $100 million per month to more than $13 billion in December 2025 alone (Covers.com, 2026).

1.2 The 2024 Election as Inflection Point

The 2024 U.S. Presidential Election served as the definitive proof of concept for the industry. While traditional polling models described the race as a toss-up until election night, prediction markets on both Kalshi and Polymarket moved to a decisive approximately 60% probability for a Donald Trump victory weeks in advance, a divergence from conventional polling that drew widespread media coverage (Financial Content, 2026). The $3.3 billion wagered on Trump vs. Harris alone on Polymarket transformed the platform from a crypto niche product into a household name (FalconX, 2026).

That single event reshaped public perception of prediction markets. The “gambling stigma” that had long constrained the industry began to erode as audiences recognized that financially incentivized forecasting could outperform expert opinion. A Bernstein research report subsequently framed prediction markets as an emerging asset class, and media organizations across the spectrum began integrating market probabilities into their reporting infrastructure (The New Yorker, 2025).

1.3 Sports as the Volume Driver

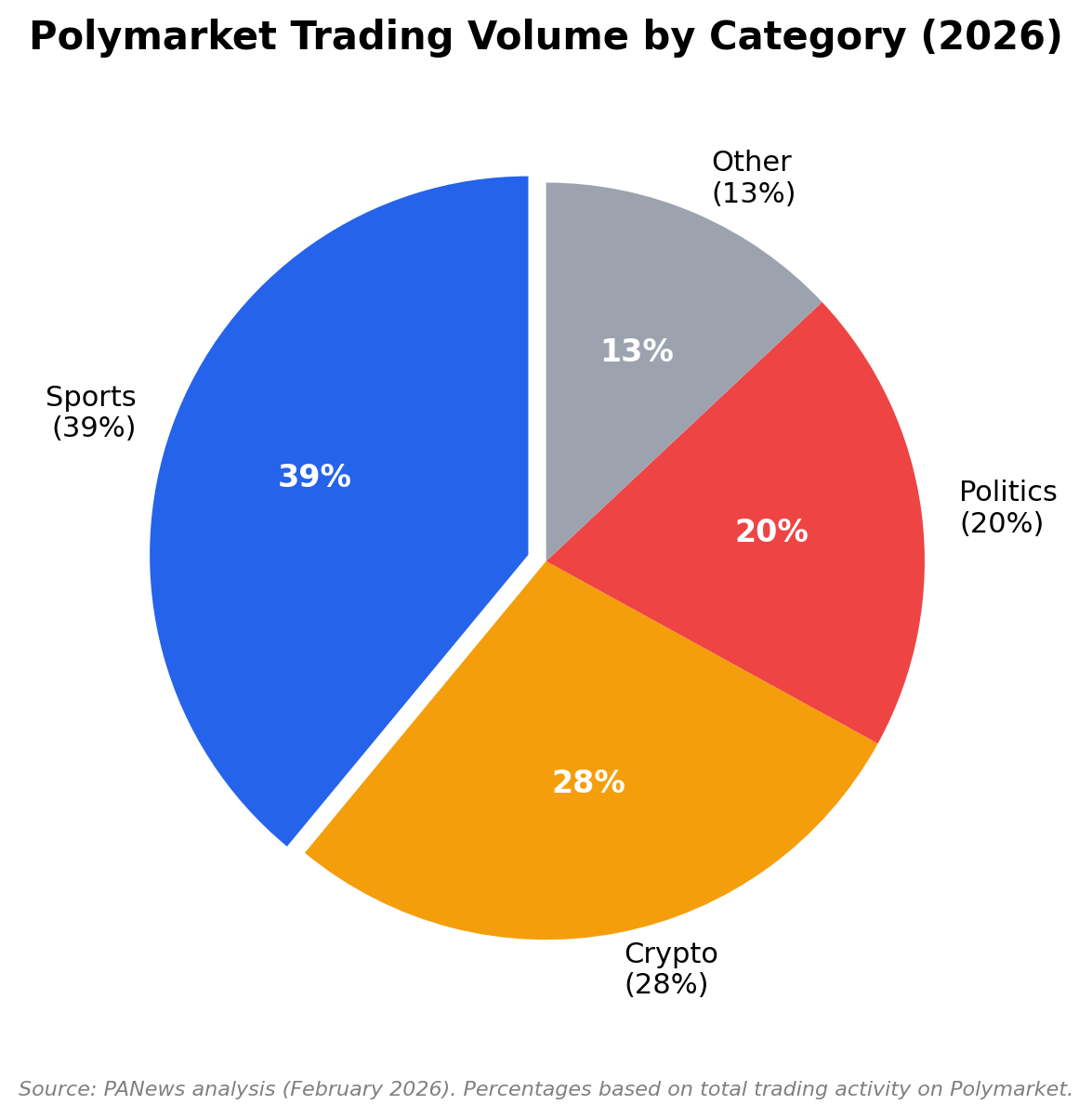

The political cycle that launched the industry into prominence has since been overtaken by sports as the primary volume driver. Sports event contracts now account for more than 80% of prediction market trading activity globally, according to data from Next.Io cited by Covers.com (2026). The Super Bowl in February 2026 generated over $6 billion in prediction market volume, including a single-day record exceeding $1 billion on game day (Covers.com, 2026). This shift from politics to sports has dramatic implications for both the regulatory environment and the competitive dynamics between the two leading platforms.

Section 2: Kalshi: The Regulated Exchange

2.1 Origins and Structure

Kalshi was founded in 2020 by Tarek Mansour and Luana Lopes Lara, both MIT graduates, with a thesis that prediction markets could be built on legitimate regulatory foundations from the outset. The company applied for and received designation as a CFTC-regulated Designated Contract Market (DCM) in 2020, a status that places it within the same regulatory framework as traditional commodity exchanges. This foundational decision shaped every subsequent element of the business: its fiat-denominated settlement, its domestic user focus, its institutional investor appeal, and its willingness to litigate aggressively against state regulators who attempt to override federal authority.

Early backers included some of Silicon Valley’s most prestigious venture firms: Paradigm, Andreessen Horowitz, and Sequoia. These investors signaled confidence that prediction markets could occupy a legitimate place in the financial system rather than remaining at its periphery (Yahoo Finance/CryptoProwl, 2026).

2.2 Business Model and Revenue

Kalshi operates as a traditional exchange, earning revenue primarily through transaction fees on contracts traded. The effective take rate is approximately 1% of contract value, as estimated by Sacra research. Users also accrue interest on cash balances and open positions, a feature that adds a financial services dimension to what might otherwise be perceived as a pure wagering platform.

The revenue trajectory has been exceptional. Kalshi reported $263.5 million in fee revenue for 2025 and reportedly surpassed that figure in early 2026 alone (Yahoo Finance, 2026). At the time of its March 2026 funding round, the company’s annualized revenue was reported at approximately $1.5 billion (CryptoProwl, 2026), implying a revenue multiple relative to valuation that is aggressive even by technology standards but consistent with the explosive volume growth underlying it.

In February 2026 alone, Kalshi’s trading volume surpassed $10 billion, representing a 12x increase from six months prior. January 2026 volume reached $9.5 billion (FalconX, 2026), putting Kalshi roughly on par with Polymarket in open interest terms, with both platforms sitting at approximately $400 million in open interest as of January 31, 2026.

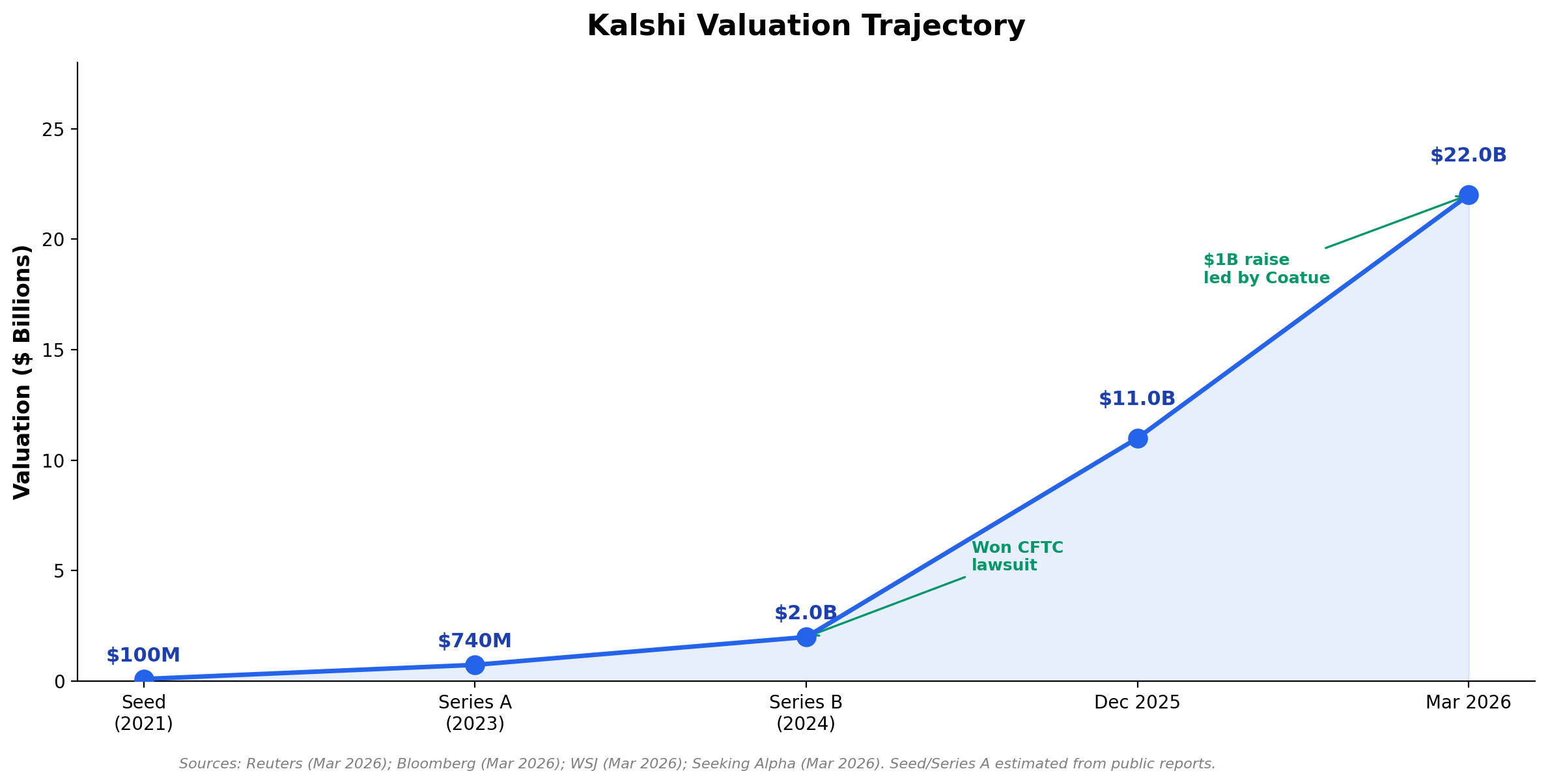

2.3 Valuation and Funding

Kalshi’s valuation has risen dramatically in a compressed timeframe. In December 2025, the company raised at an $11 billion valuation. By March 2026, a new round led by Coatue Management raised over $1 billion and nearly doubled the valuation to $22 billion (Bloomberg, 2026; Reuters, 2026; WSJ, 2026). This trajectory, from startup to a $22 billion valuation in six years, reflects both the scale of the market opportunity and investor confidence in Kalshi’s regulatory positioning as a defensible competitive advantage.

2.4 The Robinhood Partnership

One of Kalshi’s most strategically significant moves has been its partnership with Robinhood, announced in March 2025 with the launch of the Prediction Markets Hub. The partnership expanded in August 2025 to include NFL and college football contracts, giving Kalshi access to Robinhood’s tens of millions of retail users across the United States (Yahoo Sports, 2025).

Robinhood operates as a Futures Commission Merchant (FCM), meaning it facilitates access to Kalshi’s contracts without creating its own prediction markets. During Robinhood’s Q2 2025 earnings call, the company reported that one billion contracts were traded in the three months ending June 2025, with Robinhood generating approximately $10 million in revenue from event contracts in that quarter (Yahoo Sports, 2025). Analysis from InGame suggested this represented over half of Kalshi’s total trading volume for that period, making Robinhood the single largest distribution channel for Kalshi’s products.

The partnership is transformative for Kalshi’s retail strategy: it provides a compliant, nationally distributed channel that bypasses the state-by-state regulatory battles affecting direct consumer access. The Robinhood integration positions Kalshi’s contracts as financial instruments within a regulated brokerage environment, reinforcing the federal derivatives framing that sits at the core of Kalshi’s legal defense.

2.5 Market Integrity Enforcement

As part of its regulatory credibility strategy, Kalshi has demonstrated a willingness to enforce market integrity rules publicly. In February 2026, the company disclosed two insider trading cases, including a landmark action against Artem Kaptur, a video editor for MrBeast, who exhibited “near-perfect trading success” on MrBeast-related markets and was found to have traded on non-public information obtained through his employment (NPR, 2026). Kaptur received a two-year platform suspension, a $20,000 fine, and was referred to the CFTC. Beast Industries subsequently fired Kaptur following an independent investigation (Associated Press, 2026).

A separate case involved Kyle Langford, a former longshot candidate for California governor, who publicly announced a bet on himself in what appeared to be a publicity stunt. Langford was banned from the platform for five years and fined $2,200. Kalshi reported conducting over 200 insider trading investigations in the prior year, with 12 still open at the time of disclosure. The enforcement actions serve a dual purpose: they protect market integrity and they demonstrate to regulators and media partners that Kalshi takes its exchange obligations seriously.

Section 3: Polymarket: The Crypto-Native Disruptor

3.1 Origins and Structure

Polymarket was founded in 2020 by Shayne Coplan, then 22 years old, on a fundamentally different premise from Kalshi. Rather than seeking regulatory approval from the outset, Polymarket built on the Polygon blockchain, using USDC as collateral, and operated as a decentralized protocol. This architecture allowed Polymarket to offer deep, globally accessible liquidity without the licensing overhead of a traditional exchange, but it came at the cost of regulatory compliance with U.S. law.

In 2022, that cost materialized: Polymarket settled with the CFTC, paying a $1.4 million fine, and was forced to block U.S. users, effectively exiling the platform offshore for nearly four years (Investopedia, 2025). During that period, Polymarket built an international user base, developed its liquidity infrastructure, and waited for a regulatory environment that might permit its return.

3.2 The Zero-Fee Strategy and Volume Dominance

Polymarket’s most distinctive strategic choice has been its zero-fee model. Through 2025, the platform earned essentially no protocol revenue, sacrificing near-term monetization in exchange for maximum liquidity and user growth. The strategy produced extraordinary volume results: $21.5 to $22 billion in total trading volume in 2025, accounting for nearly half of global prediction market volume (PANews, 2026). January 2026 set a monthly record at $12 billion (PANews, 2026).

The zero-fee approach has a well-established precedent in technology: sacrifice revenue to dominate market share, then monetize the installed base later. The risk is that volume leadership built on zero fees is structurally fragile; it does not necessarily translate to durable competitive advantage if users are indifferent to platform and simply seek the lowest cost. Polymarket is now beginning the difficult process of testing whether its brand and liquidity depth are sticky enough to survive fee introduction.

3.3 Revenue Transition and Token Plans

In January 2026, Polymarket introduced its first revenue-generating product: a “Taker Fee” on cryptocurrency 15-minute price change markets, with rates reaching up to 3%. The impact was immediate. By early February 2026, weekly fee revenue from this single product category exceeded $1.08 million, with the 15-minute market contributing $787,000 in one week in January alone (PANews, 2026). In February 2026, Polymarket extended fee pilots to sports markets, starting with NCAA basketball and Italian Serie A, with plans to expand across all sports.

The longer-term revenue strategy centers on a planned POLY token launch, which analysts expect to generate more than 90% of Polymarket’s future revenue (PANews, 2026). Token economics would allow Polymarket to monetize platform activity through mechanisms beyond simple transaction fees, including governance participation, liquidity incentives, and token appreciation. The token strategy is consistent with Polymarket’s crypto-native DNA and offers a monetization path unavailable to traditionally regulated exchanges like Kalshi.

3.4 Return to the United States

Polymarket’s U.S. reentry has been methodical. The company acquired QCEX for $112 million, a CFTC-licensed derivatives exchange, and used that acquisition to secure formal CFTC approval in September 2025 (Bitcoin Magazine, 2025). A beta U.S. platform launched in November 2025. The returning U.S. platform offers a fee of just 0.01%, approximately 100 times lower than Kalshi’s effective take rate of approximately 1%, positioning Polymarket as an aggressive price competitor in the domestic market (PANews, 2026).

3.5 The ICE Investment and Institutional Credibility

In October 2025, Intercontinental Exchange (ICE), the parent company of the New York Stock Exchange, invested $2 billion into Polymarket at an $8 billion pre-money valuation, establishing an implied post-money valuation of approximately $9 billion (Whales Market, 2025; Bitcoin Magazine, 2025). That a company of ICE’s stature, which operates the world’s most prominent equity exchange, committed capital at this scale signals a fundamental shift in institutional perception of prediction markets. Secondary market implied valuations rose further, reaching $11.6 billion as of January 2026 (PM Insights, 2026).

Other notable investors include Founders Fund, Dragonfly Capital, Vitalik Buterin, and 1789 Capital, the venture fund backed by Donald Trump Jr. (Bitcoin Magazine, 2025). The investor roster spans both traditional finance and crypto-native capital, giving Polymarket a unique position at the intersection of the two worlds its platform was built to bridge.

3.6 Market Concentration and Profit Distribution

Polymarket’s volume leadership masks a significant structural asymmetry in how profits are distributed. Of the platform’s approximately 1.7 million wallet addresses, only 30% are profitable. More strikingly, the top 0.04% of users captured 70% of the $3.7 billion in realized gains recorded through 2025, and the top 0.23% of wallets account for 63% of all-time trading volume (FalconX, 2026). This extreme concentration suggests that Polymarket’s liquidity is largely driven by a small class of sophisticated “sharp” traders who operate at scale, rather than a broad retail base. Whether this is a strength, providing deep liquidity and accurate pricing, or a vulnerability, creating dependence on a thin layer of sophisticated users, is an open analytical question.

Section 4: Business Model Comparison

The table below provides a direct comparison of the two platforms across key structural dimensions.

| Dimension | Kalshi | Polymarket |

|---|---|---|

| Founded | 2020 | 2020 |

| Founders | Tarek Mansour, Luana Lopes Lara (MIT) | Shayne Coplan |

| Regulatory Status | CFTC-designated DCM (since 2020) | CFTC-approved via QCEX acquisition (Sept. 2025); formerly offshore |

| Settlement Currency | USD (fiat) | USDC (stablecoin on Polygon blockchain) |

| Fee Model | ~1% effective take rate (transaction fees) | 0% through 2025; 0.01% on U.S. platform; up to 3% on crypto markets |

| 2025 Trading Volume | ~$50B annualized by late 2025 (FalconX) | $21.5B total for 2025 |

| January 2026 Volume | $9.5 billion | $12 billion |

| Open Interest (Jan 31, 2026) | ~$400 million | ~$400 million |

| 2025 Revenue | $263.5 million in fees | Effectively $0 (zero-fee model) |

| Annualized Revenue (2026) | ~$1.5 billion (per funding round data) | Early fee pilot generating >$1.08M/week (Feb. 2026) |

| Valuation | $22 billion (March 2026) | $9B (ICE round); $11.6B secondary implied (Jan. 2026) |

| Latest Fundraise | $1B led by Coatue Management (March 2026) | $2B from ICE at $8B pre-money (Oct. 2025) |

| Key Investors | Coatue, Paradigm, a16z, Sequoia | ICE, Founders Fund, Dragonfly, Vitalik Buterin, 1789 Capital |

| Distribution Partners | Robinhood, CNN, CNBC | Dow Jones (WSJ, Barron’s, MarketWatch), CBS/Golden Globes, X/xAI |

| User Geography | U.S.-focused, fiat users | Global crypto users; U.S. beta (Nov. 2025) |

| Token Strategy | None | POLY token launch planned; expected to drive 90%+ of future revenue |

| Sports Share of Volume | Over 80% (consistent with industry average) | 39% sports, 28% crypto, 20% politics |

| Profit Distribution | Not publicly disclosed | Top 0.04% of users captured 70% of $3.7B in realized gains |

| Key Legal Events | Won vs. CFTC (2024); faces state criminal charges (2026) | Paid $1.4M CFTC fine (2022); returned to U.S. with CFTC approval (2025) |

Section 5: The Regulatory Battlefield

5.1 Kalshi’s Landmark CFTC Victory

The regulatory history of prediction markets in the United States is, in many ways, the history of Kalshi’s legal strategy. In 2024, Kalshi won a landmark lawsuit against the CFTC itself, securing a district court decision that granted summary judgment in Kalshi’s favor and vacated the CFTC’s ban on political event contracts (CNBC, 2026). This ruling established that Kalshi’s contracts are federally regulated derivatives, not gambling, and that the CFTC has authority over them. The victory opened the door to a rapid expansion of Kalshi’s market offerings, including sports contracts and political events, precisely the categories that have since driven explosive volume growth.

5.2 The Federal Preemption Question

The central legal question now facing the industry is whether the CFTC’s designation of prediction market contracts as derivatives preempts state gambling laws. Kalshi’s position is that as a federally licensed exchange offering CFTC-regulated swaps, state gaming regulations simply do not apply. The CFTC, under the Trump administration, has aligned itself with this view: the agency filed an amicus brief in February 2026 defending its “exclusive jurisdiction” over event contracts and arguing that state laws are preempted by the federal Commodity Exchange Act (CEA) (ESPN, 2026).

State regulators and courts have not uniformly accepted this framework. The resulting legal landscape is a patchwork of conflicting rulings that has created profound operational uncertainty for the industry.

5.3 State-Level Battles

The state-level legal battles involving Kalshi’s sports contracts in 2025 and 2026 illustrate the depth of judicial disagreement on these questions.

- Massachusetts: In March 2026, the state won an injunction barring Kalshi from offering sports contracts to Massachusetts residents. The court explicitly rejected Kalshi’s CFTC preemption argument, holding that state gambling laws remain applicable despite the federal regulatory framework (ESPN, 2026).

- Nevada: A federal court dissolved Kalshi’s preliminary injunction in November 2025, allowing Nevada to enforce its gaming laws against the platform.

- Tennessee: In February 2026, Kalshi won a preliminary injunction, with the court finding that sports event contracts are likely “swaps” under the CEA and therefore subject to federal, not state, jurisdiction (ESPN, 2026).

- Arizona: In March 2026, Arizona became the first state to file criminal charges against Kalshi, a 20-count charging document alleging illegal gambling and election betting violations. Kalshi preemptively filed a federal lawsuit against Arizona to halt the charges (New York Times, 2026; CNBC, 2026; ESPN, 2026).

5.4 The Gambling Versus Derivatives Debate

The core dispute is a genuine legal ambiguity, not a simple question of bad-faith enforcement. Prediction market contracts share structural features with both derivatives and gambling instruments. They are priced between one cent and 99 cents, representing the probability-weighted expectation of a binary outcome, which is economically equivalent to an option’s intrinsic value. They are settled based on real-world events, cleared through a regulated exchange, and held by users with hedging or speculative motivations. These features support the derivatives classification.

At the same time, the user experience is functionally identical to sports betting: a user selects a team, enters an amount, and collects a payout if the team wins. State gaming regulators argue that the underlying economic function, wagering on sporting outcomes, is gambling regardless of the regulatory vehicle through which it is offered. The courts are deeply divided, and absent a definitive appellate ruling or Congressional clarification, the legal landscape will remain uncertain for years.

This uncertainty is arguably Kalshi’s greatest risk. A company valued at $22 billion on the basis of sports contract volume could face significant operational disruption if courts consistently reject the federal preemption argument in major states. Conversely, a Supreme Court ruling or federal legislation affirming CFTC preemption would eliminate the state-level risk entirely and represent a transformative event for the industry.

5.5 Polymarket’s Regulatory Path

Polymarket’s regulatory approach has been the inverse of Kalshi’s. Rather than building from a regulatory foundation, Polymarket accepted the consequences of its early non-compliance (the 2022 CFTC fine and forced offshore exile), then pursued a structured re-entry through the acquisition of a CFTC-licensed entity. The QCEX acquisition and subsequent CFTC approval provide Polymarket with a compliant domestic operating structure, though one that is operationally distinct from the offshore platform that built its global user base (Regulatory Oversight, 2025). Polymarket now faces a version of the same preemption question as Kalshi for its sports markets, though the company’s lower domestic profile to date has kept it out of the most aggressive state enforcement actions.

Section 6: Demographics and the Path to Mainstream

6.1 User Profiles

The two platforms serve meaningfully different user bases, a divergence that reflects their structural differences and has implications for long-term growth dynamics.

Kalshi’s user base skews toward regulated finance users: retail investors familiar with brokerage accounts, Robinhood’s existing customer base, and institutional participants comfortable with CFTC-regulated instruments. The platform’s fiat-denominated settlement and exchange-style interface make it accessible to users who have no interest in or familiarity with cryptocurrency. The Robinhood distribution channel is particularly significant here: it delivers Kalshi’s products to a demographic already engaged with financial instruments in a familiar app environment.

Polymarket’s historical user base has been crypto-native, skewing male, aged 25 to 45, concentrated in technology and finance. The platform’s use of USDC for collateral and its Polygon blockchain infrastructure have historically required at least basic crypto literacy to access. The extreme profit concentration noted above, with the top 0.04% of users capturing 70% of realized gains, suggests that Polymarket’s liquidity is largely driven by a class of sophisticated “sharp” event traders who have migrated from traditional sports betting or financial trading into prediction markets (FalconX, 2026).

Both platforms are actively working to broaden their demographic reach through media partnerships and distribution integrations, with meaningfully different strategies for doing so.

6.2 Media Partnerships and the Mainstream Moment

The integration of prediction market data into mainstream media has accelerated dramatically since late 2025, representing perhaps the most important structural shift in the industry’s public perception.

Kalshi has secured data integration partnerships with CNN, where Chief Data Analyst Harry Enten uses Kalshi’s real-time market odds to complement traditional polling during live broadcasts, and with CNBC, where a dedicated Kalshi Hub integrates economic and financial forecasts into flagship shows including Squawk Box and Fast Money (Business Insider, 2025; Financial Content, 2026). The New Yorker described the CNN partnership as a potentially transformative legitimization event for a sector long stigmatized as gambling (The New Yorker, 2025).

Polymarket’s media strategy has taken a different direction. The company secured an expansive partnership with Dow Jones, embedding market-implied probabilities across The Wall Street Journal, Barron’s, and MarketWatch, including a custom earnings calendar displaying the probability of EPS beats for companies like NVIDIA alongside traditional analyst estimates (Financial Content, 2026). Polymarket also became the official prediction partner for the 83rd Annual Golden Globes on CBS, where its markets accurately predicted 26 of 28 winners (Financial Content, 2026).

Additional mainstream integrations in early 2026 include partnerships with Interactive Brokers and Crypto.com, and Trump Media’s reported plans to launch a prediction market on Truth Social (Covers.com, 2026). Major financial firms including FanDuel, DraftKings, and Fanatics have also launched prediction market products, suggesting that the sector is transitioning from a niche dominated by two specialists to a competitive landscape involving established platforms with large existing user bases.

6.3 The Rise of InfoFi

The category label “InfoFi,” short for Information Finance, has emerged as a way to describe the broader ecosystem of financially incentivized information aggregation that prediction markets exemplify (Financial Content, 2026). The concept reframes prediction markets not as gambling platforms but as mechanisms for producing accurate probability estimates about future events, where accuracy is enforced by financial incentives. Under this framing, prediction market data becomes a public good, a real-time aggregation of informed opinion that outperforms surveys and expert forecasts on many types of questions.

The 2024 election result provided the most visible demonstration of InfoFi’s value proposition, and the Golden Globes prediction accuracy demonstrated that the principle extends beyond politics. As media organizations increasingly treat prediction market probabilities as authoritative inputs alongside traditional data sources, the social function of these platforms is shifting from entertainment to infrastructure.

6.4 Professional Sharps and the New Trader Class

A new class of professional event traders, commonly called “sharps,” has emerged alongside the industry’s growth. These participants apply the analytical rigor of systematic trading to event markets, modeling probabilities across sports outcomes, macroeconomic events, and geopolitical developments. The extreme profit concentration on Polymarket, where a tiny fraction of wallets capture the majority of gains, is largely attributable to this class. As prediction markets deepen and liquidity improves, the sharp trader ecosystem is likely to grow, potentially accelerating price discovery while simultaneously making it more difficult for casual retail participants to generate consistent returns.

Section 7: Analysis and Outlook

7.1 Competing Theories of Competitive Advantage

Kalshi and Polymarket are not just competing for users; they are competing to validate two different theories of how a prediction market achieves durable competitive advantage.

Kalshi’s theory is that regulatory legitimacy is the moat. By being the only major prediction market with CFTC designation from inception, Kalshi can offer its products through traditional brokerage channels, attract risk-averse institutional capital, and make the case to media partners that its data is credible and compliant. Its aggressive litigation against state regulators is not simply defensive: it is an attempt to establish federal preemption as settled law, which would eliminate the compliance overhead that currently constrains the business and would provide a structural barrier to any competitor unwilling to absorb the same legal costs.

Polymarket’s theory is that liquidity and network effects are the moat. A prediction market is most valuable when it has the deepest order book, the tightest spreads, and the most accurate prices. Polymarket’s zero-fee strategy attracted the sophisticated traders who provide that liquidity, creating a flywheel: better liquidity attracts more volume, which attracts more liquidity. The planned POLY token launch would then monetize this accumulated network value without requiring the platform to compete on fee structure with regulated exchanges.

7.2 Sustainability of Each Model

Kalshi’s model is sustainable if, and only if, the legal questions around federal preemption are resolved favorably. A Kalshi valued at $22 billion is implicitly betting that CFTC jurisdiction over sports event contracts will be upheld in federal courts. If Massachusetts-style rulings proliferate, restricting Kalshi’s sports contracts in populous states, the volume assumptions underlying that valuation become questionable. The company’s cash position following the $1 billion March 2026 raise provides meaningful runway to sustain litigation across multiple states simultaneously, but legal uncertainty at this scale introduces operational and reputational risks that pure financial metrics do not fully capture.

Polymarket’s model is sustainable if the transition from zero fees to a monetized token economy is executed without material user attrition. The early evidence from the crypto market fee pilot is encouraging: $1.08 million in weekly revenue from a single product category suggests significant monetization potential. However, the 0.01% fee on the U.S. platform is extraordinarily low, and the platform’s revenue will depend heavily on the token launch’s success. Token launches in crypto markets are notoriously volatile in both price and community reception, and a poorly received launch could damage Polymarket’s reputation with the sophisticated community on which its liquidity depends.

7.3 Who Wins the Mainstream Race

On a two to three year horizon, Kalshi appears better positioned to capture the mainstream retail market in the United States. Its Robinhood distribution gives it access to a user base orders of magnitude larger than its current active trading community, within a familiar financial services interface. Its CNN and CNBC media partnerships ensure brand visibility with exactly the demographic that watches financial television and considers itself an investor rather than a gambler. If federal preemption holds in courts, the regulatory risk premium embedded in Kalshi’s valuation evaporates, and the $22 billion figure may look conservative against the backdrop of a $325 billion annual volume market.

Polymarket’s competitive strengths are more global than domestic. Its existing user base, built over four years of offshore operation, represents a deep well of sophisticated international liquidity that Kalshi cannot easily replicate. The ICE investment provides institutional credibility and potential integration pathways with traditional financial infrastructure. And the planned token launch, if successful, could create a self-reinforcing economic flywheel that traditional fee-based exchanges simply cannot match.

The most likely medium-term outcome is not a single winner but a bifurcated market: Kalshi dominating U.S. retail and institutional flows within regulated brokerage channels, and Polymarket dominating the global crypto-native market and the high-frequency sharp trading ecosystem. Whether these two segments remain distinct, or whether regulatory harmonization and product evolution bring them into direct competition, will be one of the defining questions of financial markets in the late 2020s.

7.4 Systemic Risks and Open Questions

Several risks and open questions deserve explicit acknowledgment. First, the prediction market industry’s explosive growth has occurred largely without a major market failure or manipulation scandal at scale. As volumes grow toward the hundreds of billions, the consequences of successful manipulation or flash crashes in illiquid markets become more systemic. Both Kalshi’s enforcement infrastructure and Polymarket’s decentralized architecture will be tested in ways they have not yet faced.

Second, the concentration of profits among a small number of sophisticated traders raises questions about the social function of prediction markets at scale. If retail participants consistently lose to sharp professionals, the political sustainability of the industry’s regulatory treatment may come under pressure, particularly from legislators who currently view it as a consumer finance innovation rather than a professional speculation venue.

Third, the convergence of prediction markets with sports betting economics is creating business models that blend financial regulation, gaming regulation, and media economics in ways that existing regulatory frameworks were not designed to handle. The resolution of these boundary questions, through litigation, legislation, or regulatory guidance, will shape the industry’s structure for the next decade.

What is not in question is the scale of the opportunity. A market that grew from under $16 billion to $64 billion in a single year, and that is on pace to exceed $325 billion in the next, represents one of the most significant emergent financial categories of the current decade. Both Kalshi and Polymarket have positioned themselves at its center, with fundamentally different but internally coherent strategies for capturing it.

References

- FalconX. (2026). From Opinions to Odds: Emerging Trends in the Prediction Market Landscape. https://www.falconx.io/newsroom/from-opinions-to-odds-emerging-trends-in-the-prediction-market-landscape

- Bloomberg. (2026, March 20). Kalshi Gets $1 Billion in New $22 Billion Funding Round. https://www.bloomberg.com/news/articles/2026-03-19/kalshi-gets-1-billion-in-new-funding-at-22-billion-valuation

- Reuters. (2026, March 20). Kalshi valued at $22 billion in latest funding round, WSJ reports. https://www.reuters.com/business/kalshi-secures-22-billion-valuation-latest-funding-round-wsj-reports-2026-03-19/

- The Wall Street Journal. (2026, March 20). Kalshi Cinches $22 Billion Valuation in Ongoing Round. https://www.wsj.com/articles/kalshi-cinches-22-billion-valuation-in-ongoing-round-194007ac

- Yahoo Finance / CryptoProwl. (2026, March 21). Kalshi’s Valuation Doubles To $22 Billion In New Funding Round. https://finance.yahoo.com/markets/options/articles/kalshi-valuation-doubles-22-billion-200400844.html

- ESPN. (2026, March 18). Arizona first state to file criminal charges against Kalshi. https://www.espn.com/sports-betting/story/_/id/48234770/arizona-first-state-file-criminal-charges-kalshi

- CNBC. (2026, March 17). Arizona charges Kalshi with criminal misdemeanors, alleging illegal gambling. https://www.cnbc.com/2026/03/17/arizona-kalshi-criminal-misdemeanor-charges.html

- The New York Times. (2026, March 18). Arizona Files Criminal Charges Against Kalshi, the Prediction Site. https://www.nytimes.com/2026/03/17/technology/arizona-criminal-charges-kalshi.html

- NPR. (2026, February 25). Kalshi reveals insider trading case against editor for MrBeast. https://www.npr.org/2026/02/25/nx-s1-5726050/kalshi-insider-trading-enforcement-actions

- Associated Press. (2026, March 5). MrBeast fires a video editor over insider trading accusations by Kalshi. https://apnews.com/article/mrbeast-jimmy-donaldson-kalshi-7a8bb7e2aecee7428bcc2dd1eb08ac67

- Yahoo Sports. (2025, August 19). Robinhood To Offer Kalshi’s Football Event Contracts. https://sports.yahoo.com/article/robinhood-offer-kalshi-football-event-212638324.html

- Business Insider. (2025, December 4). Kalshi Strikes Deal With CNBC, Days After CNN Partnership. https://www.businessinsider.com/kalshi-cnbc-deal-cnn-data-integration-partnership-2025-12

- The New Yorker. (2025, December 12). America’s Betting Craze Has Spread to Its News Networks. https://www.newyorker.com/news/the-lede/americas-betting-craze-has-spread-to-its-news-networks

- Bitcoin Magazine. (2025, November 25). Polymarket Receives Approval From CFTC For Official U.S. Return. https://bitcoinmagazine.com/business/polymarket-receives-cftc-approval

- Investopedia. (2025, November 25). Polymarket Just Got CFTC Sign-Off. Prediction Markets Are on the March. https://www.investopedia.com/polymarket-just-got-cftc-sign-off-prediction-markets-are-on-the-march-kalshi-sports-betting-11857212

- Regulatory Oversight. (2025, December 4). CFTC Approval Allows Polymarket to Reenter the U.S. Market. https://www.regulatoryoversight.com/2025/12/cftc-approval-allows-polymarket-to-reenter-the-u-s-market/

- PANews. (2026, February 18). Is Polymarket rushing to issue cryptocurrency to boost revenue? https://www.panewslab.com/en/articles/019c6c19-555c-7603-a59a-1d68c381bcf4

- Covers.com. (2026, March 13). Prediction Market Volume Quadrupled in Past 2 Years, Report Finds. https://www.covers.com/industry/prediction-market-volume-quadrupled-in-past-two-years-report-finds-march-13-2026

- Financial Content / PredictStreet. (2026, February 1). Betting on the News: How Prediction Markets Are Redefining Mainstream Media. https://markets.financialcontent.com/buffnews/article/predictstreet-2026-2-1-betting-on-the-news-how-prediction-markets-are-redefining-mainstream-media

- Whales Market. (2025, December 28). How High Will Polymarket’s Mindshare Go? https://whales.market/blog/how-high-will-polymarkets-mindshare-go/

- Gaming Intelligence. (2025, August 21). Robinhood debuts NFL and college football prediction markets. https://www.gamingintelligence.com/sectors/betting/218489-robinhood-debuts-nfl-and-college-football-prediction-markets/