A DuPont analysis of Signify NV reveals a global lighting leader navigating simultaneous headwinds: declining conventional revenues, intensifying price competition, and a CEO transition that leaves 2026 as a defining year for the company’s strategic direction.

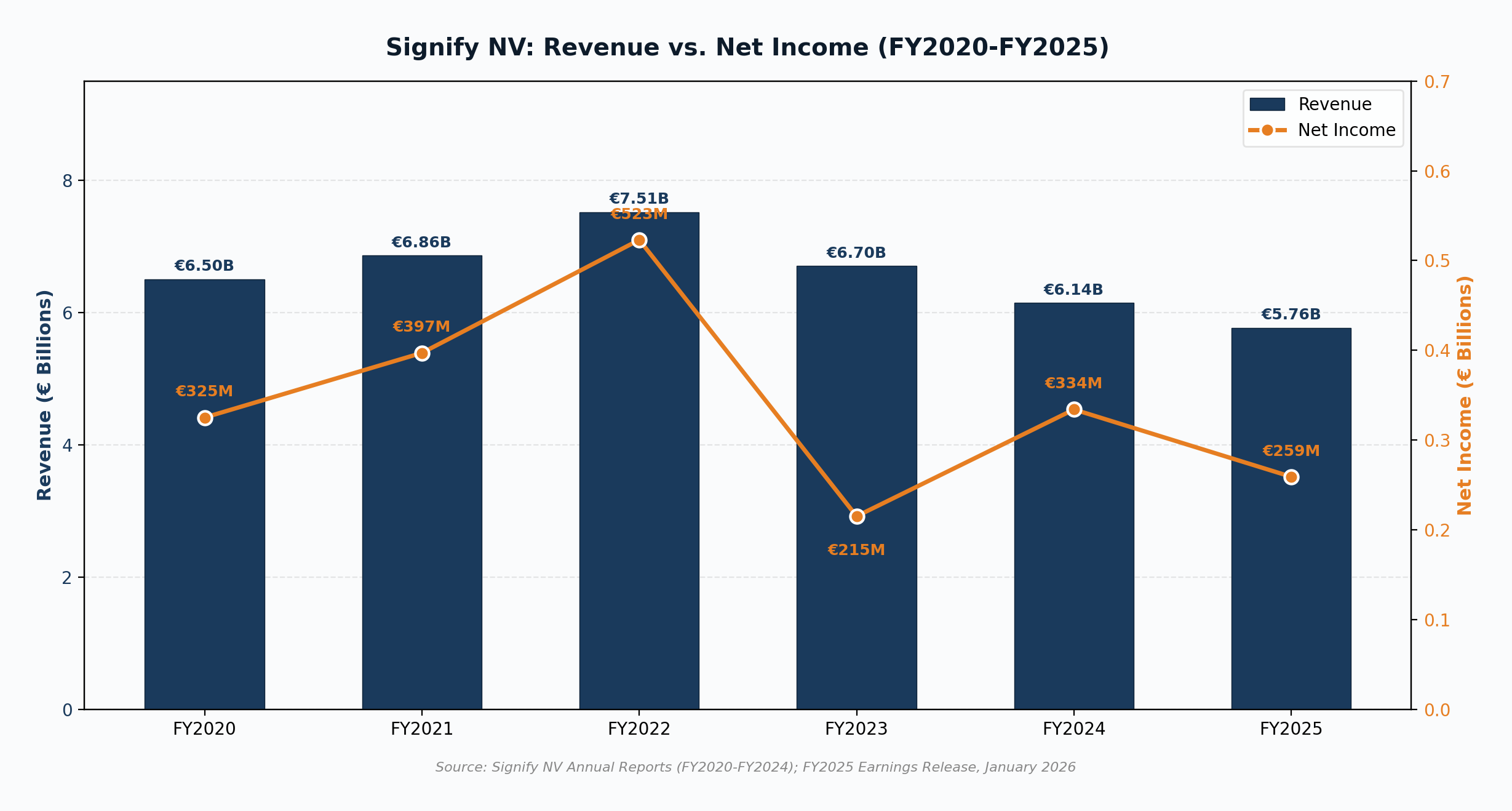

Signify NV (Euronext: LIGHT), formerly Philips Lighting, closed its fiscal year 2025 with €5,765 million in sales, a 3.4% decline on a comparable basis, and the third consecutive year of revenue contraction since the company’s FY2022 peak of €7.5 billion (Signify, 2026a). The world’s largest lighting company by revenue is simultaneously managing the structural decline of its conventional lighting business, fighting price pressure in commoditized LED categories, and betting its future on connected lighting, IoT services, and circular economy revenues. This article applies the DuPont analysis framework to evaluate whether Signify’s business strategy is positioning it for sustainable growth or merely delaying an inevitable reckoning with a fragmenting global market.

Company Profile: From Philips Lighting to Digital Platform

Headquartered in Eindhoven, Netherlands, Signify operates in more than 70 markets with approximately 27,000 employees. The company’s brand portfolio spans Philips for mainstream consumer and professional lighting, Philips Hue for premium connected home solutions, WiZ for accessible smart lighting, Interact for IoT-enabled building management systems, and Color Kinetics for architectural and entertainment applications (Signify, 2026b). This multi-brand architecture enables Signify to compete across segments ranging from residential consumers to enterprise-scale building operators.

Signify operates through four business segments: Professional (the largest, focused on commercial and public lighting), Consumer (led by Philips Hue and WiZ), OEM (components and modules sold to other manufacturers), and Conventional (legacy non-LED lighting products in managed decline). The company also holds industry-leading sustainability credentials: carbon-neutral operations since 2020, a Platinum EcoVadis rating, and inclusion in the Dow Jones Sustainability World Index (Signify, 2026b).

| Metric | Value |

|---|---|

| FY2025 Revenue | €5,765 million |

| FY2025 Net Income | €259 million |

| Adjusted EBITA Margin | 8.9% |

| Free Cash Flow | €440 million (7.6% of sales) |

| Connected Light Points | 167 million installed base |

| Employees | ~27,000 across 70+ markets |

| Circular Economy Revenue | 37% of total sales (surpassed 32% target) |

The Revenue Trajectory: Three Years of Contraction

Signify’s revenue peaked at €7,514 million in FY2022, driven by strong post-pandemic demand and favorable pricing conditions across its professional and consumer segments. Since then, revenues have declined steadily: €6,704 million in FY2023, €6,143 million in FY2024, and €5,765 million in FY2025, representing a cumulative decline of 23.3% from the peak (Signify, 2026a; Signify, 2026b).

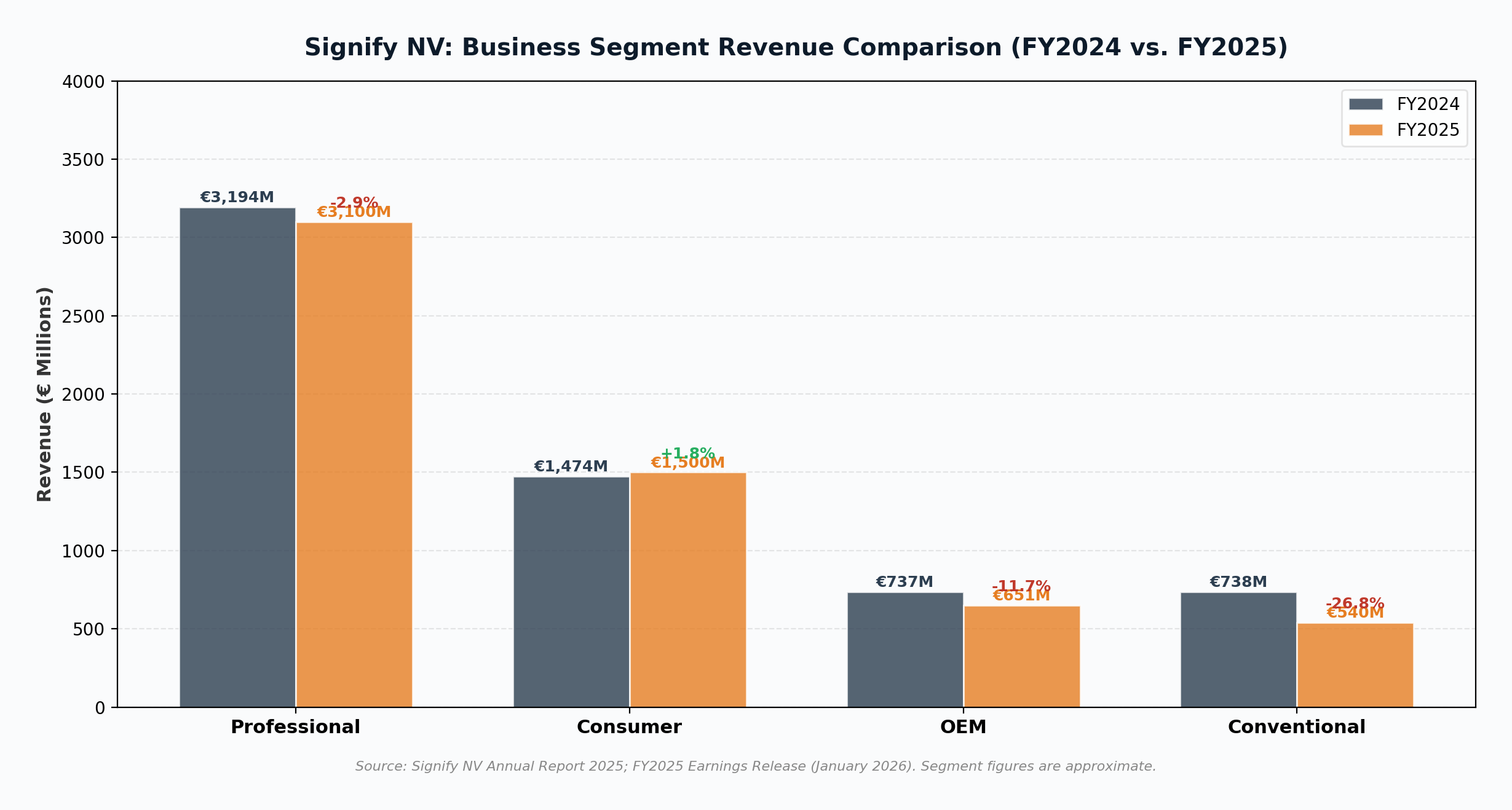

The decline is not uniform across the business. The Professional segment, representing roughly 54% of revenue, grew in the United States but declined in Europe, where public infrastructure spending remained weak in Germany, France, and the Benelux region. The Consumer segment delivered sustained growth in all regions except China, driven by the strength of the Philips Hue ecosystem. The OEM segment faced an 11.6% revenue decline due to pricing pressure and softening automotive demand. Most dramatically, the Conventional segment declined 26.8% as the market transitions away from legacy lighting technologies (Signify, 2026a).

DuPont Analysis: Profitability Recovering, Leverage Declining

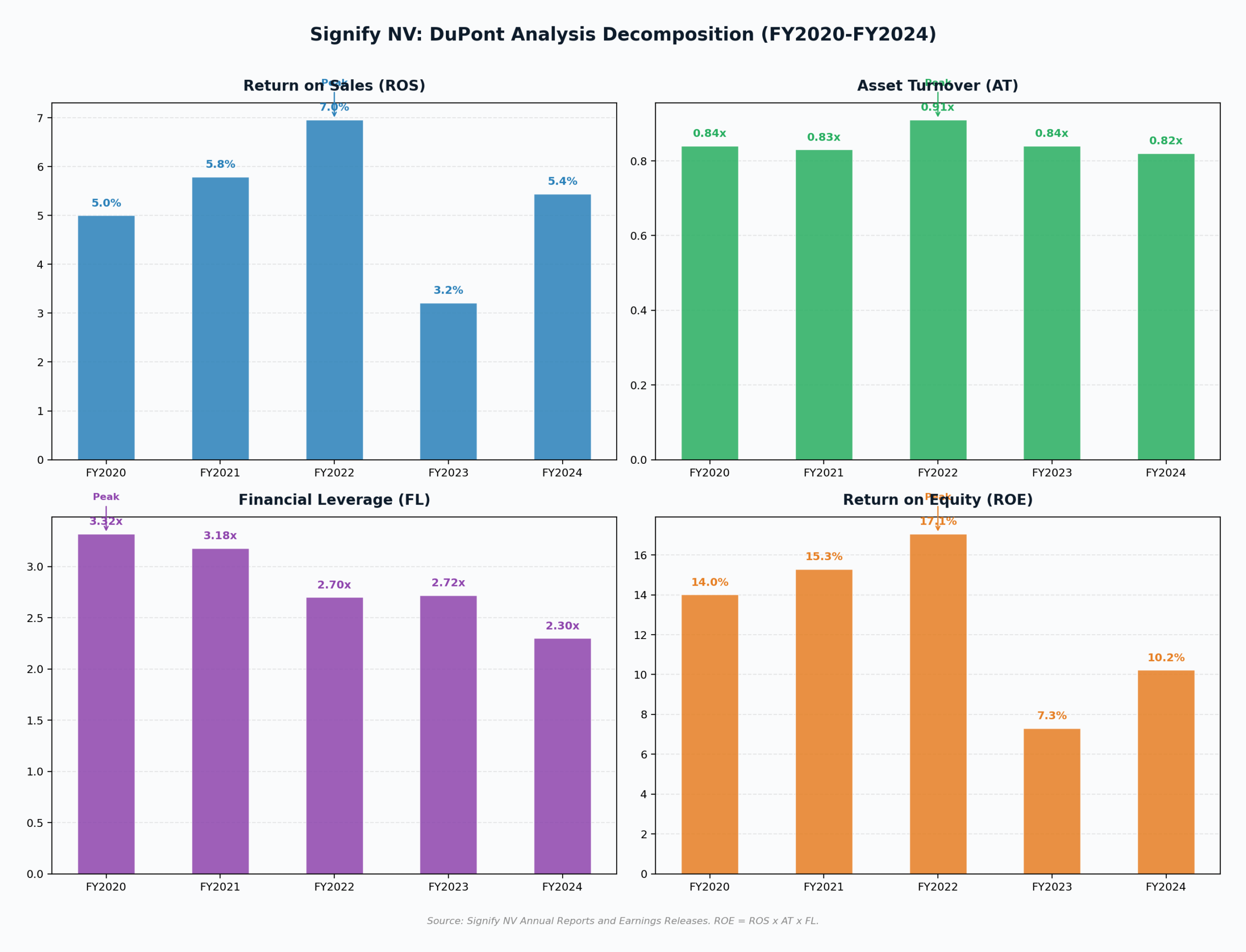

The DuPont model decomposes Return on Equity (ROE) into three components: Return on Sales (ROS), Asset Turnover (AT), and Financial Leverage (FL). Applied to Signify’s financials from FY2020 through FY2024, the decomposition reveals a complex picture where improving margins coexist with deliberate deleveraging that mechanically suppresses ROE (Hargrave, 2025).

Return on Sales: The Margin Recovery

ROS peaked at 6.96% in FY2022 during a period of strong demand and favorable pricing. It collapsed to 3.21% in FY2023 as volumes declined and restructuring charges accumulated, then recovered to 5.44% in FY2024, indicating improved margin discipline (Signify, 2026b). However, FY2025 preliminary data shows adjusted EBITA margin declining to 8.9% from 9.9%, and net income falling to €259 million from €334 million, suggesting the margin recovery has stalled as tariffs, trade channel pricing pressure, and overcapacity in commoditized LED categories take their toll (Signify, 2026a).

Asset Turnover: Remarkably Stable

Unlike many industrial companies, Signify’s Asset Turnover has remained relatively stable between 0.82x and 0.91x across the five-year period. The peak of 0.91x in FY2022 reflected strong revenue generation against a stable asset base. The current 0.82x is the lowest in the period, indicating that the revenue decline has outpaced any corresponding reduction in the asset base. Total assets declined from €8,286 million in FY2022 to €7,505 million in FY2024, a reduction of 9.4%, but revenue declined faster at 18.2% over the same period (Signify, 2026b).

Financial Leverage: Deliberate Deleveraging

The most striking trend is the steady decline in Financial Leverage from 3.32x in FY2020 to 2.30x in FY2024. Shareholders’ equity grew from €2,320 million to €3,267 million, a 41% increase, while total assets remained relatively stable. This represents a deliberate strategy to strengthen the balance sheet and reduce financial risk, even though it mechanically suppresses ROE. At FY2022 ROS and AT levels but with FY2024 leverage, ROE would have been approximately 14.5% rather than the 17.1% actually achieved (Signify, 2026b).

| DuPont Component | FY2020 | FY2022 (Peak) | FY2023 | FY2024 |

|---|---|---|---|---|

| Revenue (€M) | €6,502 | €7,514 | €6,704 | €6,143 |

| Net Income (€M) | €325 | €523 | €215 | €334 |

| ROS | 5.00% | 6.96% | 3.21% | 5.44% |

| Asset Turnover | 0.84x | 0.91x | 0.84x | 0.82x |

| Financial Leverage | 3.32x | 2.70x | 2.72x | 2.30x |

| ROE | 14.01% | 17.06% | 7.30% | 10.22% |

Strategic Pillars: Where Signify is Placing Its Bets

Connected Lighting and the Interact Platform

Signify’s installed base of 167 million connected light points represents its most significant competitive moat. The Interact platform, trusted in over 40,000 projects worldwide, enables data-driven energy optimization, space utilization analytics, and predictive maintenance for commercial buildings and cities (Signify, 2026c). Connected lighting showed strong growth in both Professional and Consumer markets during FY2025, even as non-connected categories declined. In March 2026, Signify launched next-generation Interact solutions at Light + Building, including Interact Building for intelligent indoor environments and EasyConnect for simplified outdoor smart lighting deployment (Signify, 2026c).

The strategic logic is clear: connected lighting products command higher margins than standalone luminaires, and the data services they enable create recurring revenue streams that improve both ROS and Asset Turnover. However, the transition is occurring within a broader market where overcapacity in commoditized, non-connected LED categories intensifies price competition in trade channels (Signify, 2026a).

Circular Economy and Light-as-a-Service

Circular economy revenues reached 37% of total sales in FY2025, surpassing the company’s 32% target, with strong contributions from serviceable luminaires in the Professional segment (Recolight, 2026). The Light-as-a-Service (LaaS) model converts one-time product sales into recurring service contracts, reducing upfront capital barriers for customers while generating predictable revenue streams for Signify. This model directly benefits the DuPont framework: recurring revenue stabilizes ROS, asset-light service delivery supports AT, and predictable cash flows enable more efficient capital structure management.

Key Insight

Signify surpassed its 2025 target to reduce greenhouse gas emissions across its entire value chain by 40% against the 2019 baseline, double the pace required by the Paris Agreement. These credentials are not merely reputational. As corporate, municipal, and government buyers increasingly prioritize sustainability criteria in procurement decisions, Signify’s Platinum EcoVadis rating and Dow Jones Sustainability World Index listing function as competitive differentiators that directly influence deal flow (Signify, 2026b).

The Conventional Cash Cow

The Conventional segment represents a textbook cash-cow dynamic. Revenues are declining rapidly at 26.8% as the global market transitions away from legacy lighting technologies, yet the segment maintains an 18.6% EBITA margin, generating substantial cash flows that can be reinvested into connected and IoT-driven growth areas (Signify, 2026a). This structural decline is expected and aligned with broader industry trends. The strategic question is not whether the Conventional segment will disappear, but whether Signify can replace those cash flows fast enough with higher-margin connected lighting revenues.

Competitive Landscape: Fragmented and Intensifying

While Signify remains the global leader by revenue, competition is intensifying on multiple fronts. In North America, Acuity Brands (approximately $4.2 billion in revenue) has been closing the gap: in Q1 2023, Acuity’s revenues were 63% of Signify’s, and by Q3 2025, following the acquisition of QSC, Acuity’s revenues reached 86% of Signify’s (Electrical Trends, 2025). Acuity’s Atrius IoT platform competes directly with Signify’s Interact, and Acuity’s adjusted operating margin of 20.1% in its lighting segment significantly exceeds Signify’s 8.9% adjusted EBITA margin (MatrixBCG, 2026).

In Europe, the Zumtobel Group competes in architectural and commercial lighting. In Asia-Pacific, domestic manufacturers including Opple, NVC, MLS, and Yankon exert significant price pressure in value and OEM segments, leveraging large-scale manufacturing and cost advantages (MarketsandMarkets, 2024a). This fragmented competitive landscape, combined with overcapacity in non-connected LED categories, has contributed to the margin compression visible in Signify’s recent results.

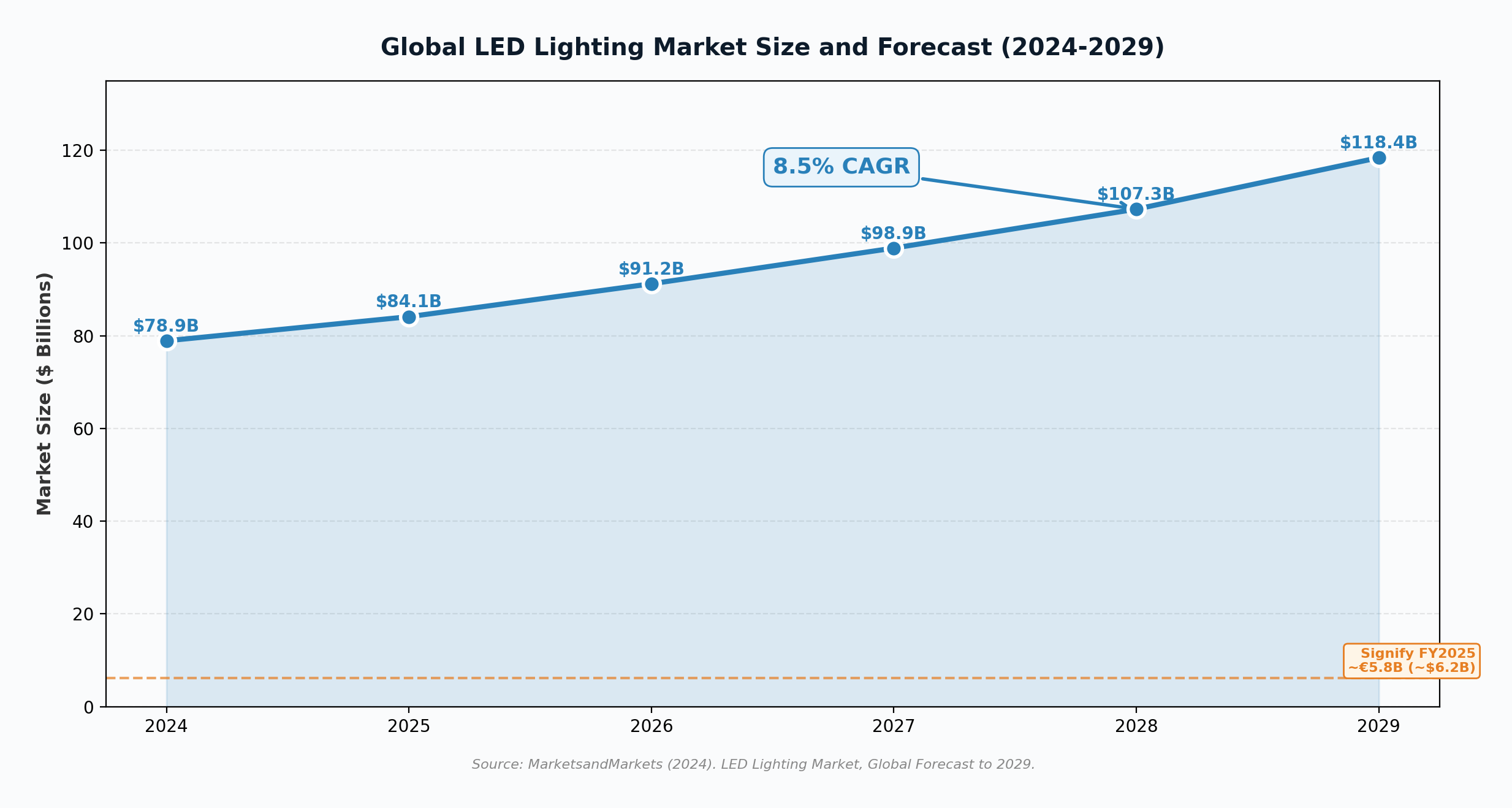

The Market Opportunity: A $118 Billion Industry by 2029

Despite Signify’s recent revenue contraction, the broader LED lighting market presents a compelling growth backdrop. The global LED lighting market was valued at $78.9 billion in 2024 and is projected to reach $118.4 billion by 2029, growing at a compound annual growth rate of 8.5% (MarketsandMarkets, 2024c). Growth drivers include smart lighting system adoption, government energy-efficiency mandates, and rising demand for IoT-enabled building management solutions.

The Asia-Pacific region is expected to grow fastest at a 10.3% CAGR, driven by urbanization, construction activity, and the digitalization of households (MarketsandMarkets, 2024c). However, this is also where Signify faces the most intense price competition from domestic Asian manufacturers.

2026: A Defining Transition Year

Signify enters 2026 under new CEO As Tempelman, who took over in September 2025 after the company cycled through three CEOs in twelve months (Inside Lighting, 2026). The company has initiated a €180 million cost reduction program that will eliminate approximately 900 positions, and is conducting a full strategy and portfolio review to be presented at its Capital Markets Day on June 23, 2026 (Signify, 2026a).

The FY2026 outlook is cautious: Signify expects an adjusted EBITA margin of 7.5% to 8.5% (below FY2025’s 8.9%) and free cash flow of 6.5% to 7.5% of sales. Notably, the company declined to provide sales guidance, citing “huge divergence” in market dynamics across its end markets (Reuters, 2026). Share repurchases for capital reduction have been paused to preserve financial flexibility during the strategic review.

Strategic Watch

The EBITA margin guidance of 7.5% to 8.5% represents the lowest since Signify’s 2016 IPO and sits approximately 150 basis points below analyst expectations (Reuters, 2026). The June Capital Markets Day will be the most consequential strategic update in the company’s history as a standalone entity.

Conclusion: A Company Between Two Eras

The DuPont analysis reveals Signify as a company caught between the declining profitability of its legacy lighting business and the emerging growth potential of its connected, IoT-driven future. The partial recovery of ROS from 3.21% in FY2023 to 5.44% in FY2024 demonstrates that margin discipline is achievable, while the deliberate reduction of Financial Leverage from 3.32x to 2.30x reflects a healthier, if less leveraged, balance sheet.

The core strategic tension is clear. Signify’s strongest growth engines, connected lighting, Interact IoT services, and circular economy revenues, are genuine differentiators in a market projected to grow at 8.5% CAGR through 2029. But these high-value categories are not yet growing fast enough to offset the combined drag from declining conventional revenues, OEM pricing pressure, and intensifying competition in non-connected LED categories.

Whether Signify emerges from its 2026 strategic review as a leaner, more focused company positioned to capture connected lighting growth, or as a legacy industrial firm managing a slow decline, will depend on the choices made at its June Capital Markets Day. The DuPont framework makes one thing clear: improvement must come primarily through ROS (margin expansion in connected and service-based categories) and AT (generating more revenue per asset through digital services), because the deliberate deleveraging that is improving balance sheet health will continue to constrain ROE mechanically. For a company sitting on 167 million connected light points, the platform is there. The question is whether the strategy can match the scale of the opportunity.

References

Electrical Trends. (2025, October 30). Acuity and Signify: Differing points of light. https://electricaltrends.com/2025/10/30/acuity-and-signify-differing-points-of-light/

Hargrave, M. (2025, July 16). DuPont analysis: Definition, uses, formulas, and examples. Investopedia. https://www.investopedia.com/terms/d/dupontanalysis.asp

Inside Lighting. (2026, January 30). Signify to cut 900 jobs amid ongoing contraction. https://inside.lighting/news/26-01/signify-cut-900-jobs-amid-ongoing-contraction

MarketsandMarkets. (2024a). Asia-Pacific smart lighting market: Competitive landscape and key players. https://www.marketsandmarkets.com/ResearchInsight/asia-pacific-smart-lighting-companies.asp

MarketsandMarkets. (2024b). North America smart lighting market: Competitive landscape and key players. https://www.marketsandmarkets.com/ResearchInsight/north-america-smart-lighting-companies.asp

MarketsandMarkets. (2024c). LED lighting market: Global forecast to 2029. https://www.marketsandmarkets.com/Market-Reports/led-lighting-market-201130554.html

MatrixBCG. (2026). What is the competitive landscape of Acuity Brands Company? https://matrixbcg.com/blogs/competitors/acuitybrands

Recolight. (2026, February 2). Circular revenues hit 37% for Signify. https://www.recolight.co.uk/circular-lighting-report/circular-revenues-hit-37-for-signify/

Reuters. (2026, January 30). Signify launches business review and cost cuts, shares slump as results miss market view. https://www.reuters.com/business/signify-launches-business-review-cost-cutting-drive-results-miss-market-view-2026-01-30/

Signify NV. (2026a, January 30). Signify’s fourth quarter and full-year results 2025 [Press release]. https://www.signify.com/global/our-company/news/press-releases/2026/20260130-signify-fourth-quarter-and-full-year-results-2025

Signify NV. (2026b). Signify annual report 2025. https://www.signify.com/static/2025/signify-annual-report-2025.pdf

Signify NV. (2026c, March 9). Next-generation Signify Interact solutions provide smarter, safer, more efficient lighting for intelligent buildings and cities [Press release]. https://www.signify.com/global/our-company/news/press-releases/2026/20260309-next-generation-signify-interact-solutions-provide-smarter-safer-more-efficient-lighting-for-intelligent-buildings-and-cities

Yahoo Finance. (2026). Signify N.V. (LIGHT.AS) company profile. https://finance.yahoo.com/quote/LIGHT.AS/profile/