Ten days ago, this publication argued that China had quietly won the humanoid manufacturing race. A new round of reporting from Hong Kong reveals the next chapter: Chinese factories can now build humanoids faster than the world can find a use for them. The story has shifted from supply to demand, and that shift matters.

On June 6, 2026, Associated Press reporters in Hong Kong and Beijing published a comprehensive update on the Chinese humanoid robotics industry that complicates a thesis this publication advanced on May 30. In that earlier analysis, AcadeResearch argued that China had hit factory-scale humanoid production before the United States, and that the next two years of the industry would be defined by who could manufacture humanoids at industrial volume. The supply-side argument remains broadly correct. What the AP reporting now adds is that demand is failing to keep up (Associated Press, 2026).

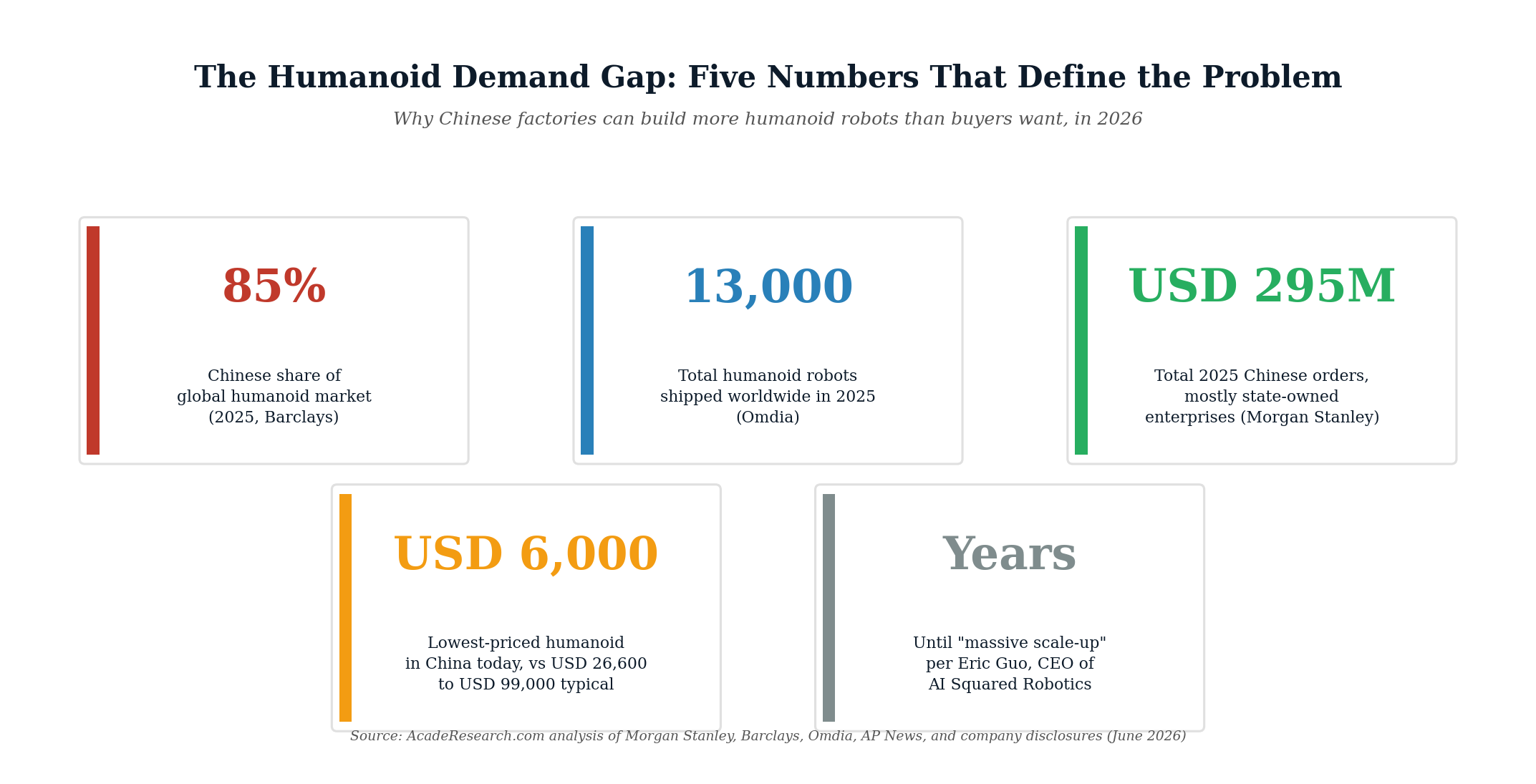

According to data compiled in the AP report and corroborated by Morgan Stanley, Barclays, and Omdia: Chinese humanoid robots accounted for approximately 85 percent of the global humanoid market in 2025; total worldwide humanoid shipments reached just over 13,000 units; total Chinese orders amounted to around 2 billion yuan, approximately $295 million; and the majority of those orders came from state-owned enterprises rather than private commercial buyers (Associated Press, 2026). These are the numbers of an industry that has built the factories but not yet built the market.

The economic question is what happens when manufacturing capacity outpaces commercial use cases. The history of consumer electronics suggests two possible outcomes: aggressive price collapse that creates new demand, or industry consolidation that destroys the marginal producer. Both are now visibly playing out in Chinese humanoid robotics, often at the same company.

Five Numbers That Define the Demand Gap

Before examining the analytical argument, the chart below collects the five most consequential data points from the AP reporting and the underlying analyst sources.

The chart below presents the same data in a comparative trajectory, showing how China’s manufacturing capacity now dwarfs both demand and US competitor output.

Three patterns are visible.

First, the volume gap between Chinese and US manufacturers is now an order of magnitude. AGIBOT and Unitree each shipped more than 5,000 humanoid robots in 2025. Figure AI and Tesla each shipped only a few hundred units in the same period (Associated Press, 2026). The factory-scale argument from May 30 is, if anything, understated.

Second, total industry shipments remain small in absolute terms. The 13,000 units shipped in 2025 is roughly equivalent to the annual output of a single mid-sized car plant operating a single shift. Morgan Stanley projects China’s humanoid sales to more than double to approximately 28,000 units in 2026, and Omdia forecasts annual shipments could surpass 1 million units by the early 2030s (Associated Press, 2026). Even those projections, if realized, would still place humanoid output well below the 70-million-unit annual scale of the global auto industry.

Third, the orders coming in are not what investors hoped for. Morgan Stanley’s 2 billion yuan order figure for 2025 sounds substantial, but the AP reports explicitly that most of those orders came from Chinese state-owned enterprises for use in power plants, data centers, and entertainment installations (Associated Press, 2026). These are not the broad commercial deployments that justify trillion-dollar market projections. They are state procurement at a scale designed to support the industry, not necessarily because the procurer needs the product.

What the Investors Are Saying

The most direct critique in the AP reporting comes from venture capitalists with money on the line. Chibo Tang of Gobi Partners, which invests in Chinese robotics startups, told the AP plainly that “the use cases of these robots are still so limited,” and that “without the demand and without that scale from the market, these companies are not able to really go into mass production” (Associated Press, 2026).

Samm Sacks, a senior fellow at the New America think tank focused on Chinese technology, characterized the industry’s structural challenge in economic terms: “The economics are tough: humanoid robots remain expensive to produce, fragile in operation, and dependent on highly structured environments to function” (Associated Press, 2026). On the prospect of consumer adoption, Sacks added that there is “a long way to go to get to a level of functionality where people will actually feel comfortable having them in their homes providing care for elderly or children.” The most plausible commercial path, in her assessment, runs through industrial and logistics settings rather than households.

Even one of the manufacturers acknowledges the constraint. Eric Guo, founder and CEO of Shenzhen-based AI Squared Robotics, told the AP that “the mass production capability in the robotic area is still at the very early stage” and that scaling up will take “years” (Associated Press, 2026). For an industry whose narrative has been built on imminent transformation, “years” is a meaningful concession.

The German-based Mercator Institute for China Studies offered a balanced framing in a recent report: Chinese humanoids are already cheaper than competitors made elsewhere, but they remain “far too expensive for widespread deployment” (Associated Press, 2026).

Why the Demand Gap Is Structural, Not Cyclical

Three structural factors explain why demand for humanoid robots has not kept pace with their increasingly impressive supply.

The first is the alternative-technology problem. Many of the industrial use cases that humanoid robotics theoretically addresses are already being handled by non-humanoid robotics. The AP reporting notes that many factories in China and elsewhere are already equipped with non-humanoid robotic arms that perform repetitive single functions, and may not need humanoid form factors at all (Associated Press, 2026). A bipedal robot is dramatically more expensive and more fragile than a stationary robotic arm that does one task well. For a factory weighing capital allocation, the humanoid is only the right answer when the work genuinely requires human-like mobility across multiple unstructured locations.

The second is what economists call the brittleness problem. Current humanoid robots perform well in carefully structured demonstration environments and fall short in messy, unpredictable real-world settings (Associated Press, 2026). Most documented commercial deployments to date involve highly choreographed tasks such as security patrols, museum guide demonstrations, dancing performances, or single-purpose package sorting. The robots can do these things. They cannot reliably do the much larger universe of tasks that would justify the $26,600-to-$99,000 price tag for most buyers.

The third is the price-versus-utility curve. The AP reports that some humanoid robots in China have reached price points below $6,000, and Morgan Stanley projects that average prices could fall to roughly $21,000 by 2050 from approximately $46,000 in 2025 (Associated Press, 2026). But price reduction alone does not solve the demand problem if the functional capability remains limited. A $6,000 humanoid that can dance but cannot reliably load a dishwasher will not find broad commercial adoption regardless of how affordable it becomes.

The State as Buyer of Last Resort

The most economically distinctive feature of the Chinese humanoid market is the role of state-owned enterprise procurement. The 2 billion yuan in 2025 orders that Morgan Stanley documented came predominantly from Chinese state-owned enterprises purchasing humanoids for power plants, data centers, and entertainment installations (Associated Press, 2026). This is structurally similar to early-stage state procurement of electric vehicles in China between 2015 and 2020, which produced both the manufacturing scale that now dominates global EV production and a substantial overhang of unsold inventory in less successful manufacturers.

The Chinese government is aware of the parallel. The AP reporting notes that “last year, the Chinese government publicly warned about the risk of a bubble in the industry given the lagging state of commercialization and applications” (Associated Press, 2026). At the same time, the 2026 to 2030 five-year plan from the ruling Communist Party explicitly targets humanoid robotics as a frontier technology priority. The Ministry of Industry and Information Technology reports that China had more than 140 humanoid robot manufacturers producing more than 330 distinct models in 2025.

The likely outcome is industry consolidation. Of those 140 manufacturers, only a handful will reach the scale and capability required to survive a market correction. Unitree, which reported 1.7 billion yuan (around $250 million) in revenue last year and a profit of more than 278 million yuan ($41 million), is one of the few profitable Chinese humanoid makers and is reportedly preparing for a Hong Kong public offering. Most of the rest are running on venture funding, state subsidies, or a combination of both (Associated Press, 2026).

The economic context. Morgan Stanley projects a $5 trillion global humanoid market by 2050. To get from 13,000 units shipped in 2025 to the millions of units annually that would justify the trillion-dollar projection, three conditions need to be met simultaneously: humanoid functional capability must improve to the point where the robots can handle unstructured environments without human supervision; unit prices must fall by another 75 percent from current levels; and commercial buyers, not state-owned enterprises, must drive the majority of orders. None of those three conditions is currently being met. All three remain plausible within the next decade. The industry’s valuation framework currently bets that all three will be met faster than any consumer or industrial technology in recent history. That bet may prove correct. It may also leave the marginal humanoid manufacturer with a factory full of inventory that has nowhere to go.

What the Demand Gap Means for the Investment Thesis

The supply-side dominance that AcadeResearch documented on May 30 remains real. China’s manufacturing infrastructure, supply chain integration, and government support have produced a humanoid industry that visibly leads the United States on production volume and is likely to maintain that lead through the end of the decade. None of the data in the AP reporting reverses that argument.

What the new reporting does is reframe the strategic question for investors and policy makers. The question is no longer who can build humanoids fastest. It is who can develop them into commercially viable products that customers will pay for without state subsidy. On that question, the AP’s reporting suggests the lead is far less clear.

The capability gap that benefits the United States, where Apple, Nvidia, Microsoft, OpenAI, and Anthropic have built the AI infrastructure that humanoid robots will eventually need to perform genuinely useful work, may matter more than the manufacturing gap that benefits China. A Unitree humanoid running an older generation of behavior models cannot solve the dexterity-and-judgment problems that prevent commercial deployment. A Figure 03 humanoid running Anthropic’s Claude or Nvidia’s Cosmos foundation model may be closer, even at one-twentieth the production volume.

The next two years of the industry will reveal whether manufacturing scale or capability quality is the binding constraint. The most likely answer is that both matter, that the two countries are competing on different dimensions of the same problem, and that the eventual market leader will need to combine Chinese-style manufacturing throughput with American-style capability development. Neither side currently has both.

The Bottom Line

Ten days ago this publication argued that China had built the humanoid factories first. That argument is correct and the AP reporting from Hong Kong has now confirmed it: Chinese manufacturers hold 85 percent of global humanoid market share, AGIBOT and Unitree shipped 5,000+ units each in 2025 against a few hundred each from Figure AI and Tesla, and Chinese state-owned enterprises placed 2 billion yuan in orders during 2025. The harder problem now visible is that the buyers are not yet there in commercial volume. Venture capitalists named in the AP reporting describe the demand side bluntly. Use cases remain limited. Robots remain brittle. Prices remain too high for widespread deployment. The Chinese government itself has warned about an industry bubble. None of this overturns the manufacturing-scale thesis. All of it complicates the investment thesis. The trillion-dollar humanoid market that Morgan Stanley projects requires three conditions: capability improvement, price reduction, and broad commercial adoption. The first two are tracking. The third is not. Whether that gap closes in five years or fifteen will determine whether Chinese humanoid factories become the next Chinese EV industry, or the next Chinese solar panel industry, where the world produced more capacity than the world ever wanted to buy.

References

Associated Press. (2026, June 6). China can build humanoids at scale. The hard part is finding enough buyers. https://apnews.com/article/china-humanoid-robots-ai-demand-7d542b5ee92caa9d79efa28de89afbbe